BREAKING: New Housing Market Data Reveals Stealth CRASH!!

The housing market isn’t just cooling down—it’s plummeting, and you don’t even know it.

The Enron Real Estate Market

Welcome, astute investors and skeptics of surface-level financial news. Do you think the real estate market is in a bubble, or perhaps, it’s resilient? Hold onto your seats because what you’re about to learn will make the Enron scandal look like child’s play.

The Mirage of Mortgage Rate Buy-Downs

Have you ever heard of a “mortgage rate buy-down?” No? Neither had I. But this under-the-radar maneuver is as important to the current real estate landscape as subprime mortgages were to the 2008 financial crisis.

Here’s the deal: some home builders are offering to “buy down” mortgage rates to make it easier for buyers to afford homes. For instance, if the prevailing mortgage rate is 8%, the builder offers to knock it down to 4% for the buyer, essentially prepaying the interest to make this possible.

Is this charity? Far from it. It’s financial engineering—smoke and mirrors—used to prop up a market that’s already in freefall.

The Illusion of Demand and Supply

“Supply, supply, supply!” That’s all you hear from the so-called experts. But what about demand? According to discussions on the ‘Forward Guidance’ podcast, demand is at an all-time low. And here’s the kicker: it would be even lower without these mortgage rate buy-downs.

So, let me ask you a rhetorical question: what happens to a market where demand is artificially propped up? Well, it’s like filling a leaky bucket. Sooner or later, you’re going to run out of water.

The Reality Behind the Numbers

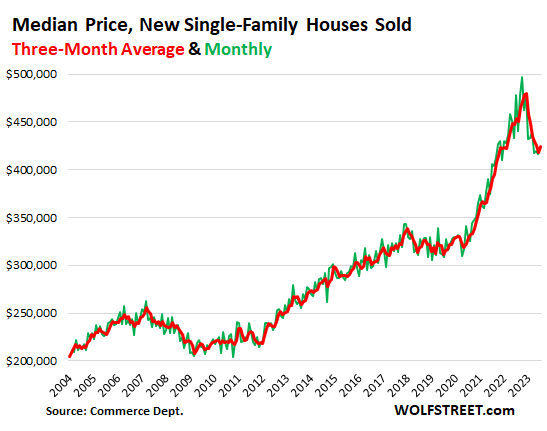

Okay, let’s break this down. On paper, a house sells for $500,000. But if the homebuilder buys down the mortgage rate, they’re effectively lowering the price without actually doing so. That same house is, in essence, sold for $450,000. It’s a mirage, people!

So why does this matter? Because it messes with the comps—the comparable sales that set the prices for entire neighborhoods. If the comps are inflated, then so is your home’s estimated value. It’s a domino effect that, when it collapses, won’t just knock down the first domino; it’ll bring down the whole table.

The Ticking Time Bomb: Unsustainable Buy-Downs

So, what happens when mortgage rates go beyond 8%? Builders can’t afford to buy down rates without digging into their margins. This means they can’t sell homes without taking a loss. It’s a ticking time bomb, and the clock is counting down fast. The real estate market is not just cooling off—it’s in a nosedive. And not just in inflation-adjusted terms. If you take away the illusion created by these mortgage rate buy-downs, even nominal prices have begun to plummet.

Don’t believe me? Look at the Case-Schiller Home Price Index. It shows a decline in housing prices since April 2022 when adjusted for inflation. But that’s just the tip of the iceberg. The real price drops are hidden, masked by this financial chicanery.

Brace Yourselves

Folks, we’re not looking at a small hiccup in the housing market. We’re staring at an impending catastrophe, a house of cards ready to topple. So, the next time you see rosy real estate data, ask yourself: is this the truth or just another Enron in the making?

Remember, accurate and honest data are the pillars of free-market capitalism. Don’t settle for Enron-style misinformation. Stay informed, stay skeptical, and most importantly, prepare for a market correction that’s not just coming—it’s already here.