AI Is Killing the Jobs That Fund the Market

How mass tech layoffs threaten the automatic payroll-driven machine that keeps the S&P 500 hitting all-time highs.

![[Section Divider Image]](https://substackcdn.com/image/fetch/$s_!EsWp!,f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2Fbdb9e53d-3712-4054-808e-50fe9fc724b2_1320x50.webp "[Section Divider Image]")

Meta: 8,000 jobs. Gone. May 20. Amazon: 30,000 gone before that. More than 113,000 tech workers cut in 2026 alone.

The official explanation is productivity. AI makes workers redundant. Efficiency is the goal. Everyone nods and moves on.

Don’t move on.

Because every one of those layoffs...and every one that follows...isn’t just a story about employment. It’s a story about the one force keeping this market at all-time highs. And that force runs on paychecks.

S&P 500 Passive Flows: Why Jobs Are the Only Number That Actually Matters

Forget PE ratios for a moment. Forget earnings guidance. Forget what the Fed said and what the yield curve is doing.

Here’s the actual reason the S&P 500 has managed to shrug off almost everything for the last thirty years and keep grinding toward new highs: every month, a fixed percentage of nearly every working American’s paycheck flows automatically into an index fund. Not discretionary. Not subject to mood or headlines or geopolitical panic. Just...automatic. Payroll comes in. The allocation goes out. Month after month, year after year.

That non-discretionary, mechanical inflow is the bid that never goes away. Geopolitical shock hits? The discretionary traders panic and sell. The market drops for two weeks. But eventually the sellers finish. And the next payroll cycle arrives. And the bid resets.

Net passive inflows: market goes up. Net passive outflows: market goes down. That’s the whole machine.

Which means the single variable that actually matters for the S&P 500’s long-term direction isn’t a Fed pivot or a tariff announcement. It’s jobs. Specifically: how many people have a paycheck to allocate this month?

And here’s the wrinkle that changes everything. Not all paychecks are created equal.

A hundred thousand white-collar workers contribute disproportionately more to passive inflows than a hundred thousand blue-collar workers. The finance professional. The software engineer. The office administrator with a 401(k) on autopilot. These are the workers who fund the machine at scale. And these are precisely the workers that AI is targeting first.

So here’s the question nobody is asking out loud: what happens to the passive bid when the white-collar workers who support it most start disappearing at scale?

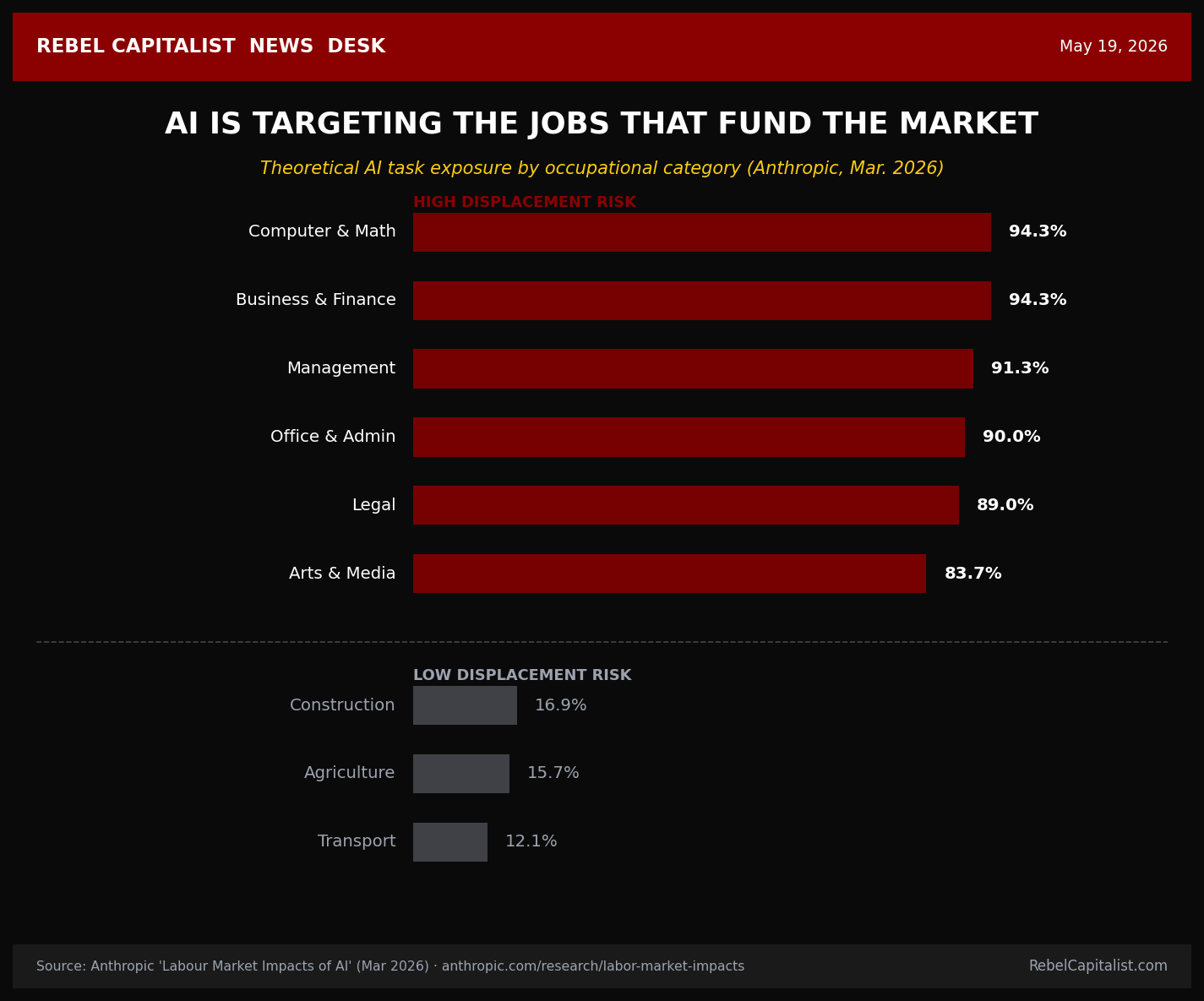

AI Job Displacement: What Anthropic’s Own Data Reveals About Which Workers Are at Risk

In February 2026, Anthropic published a labor market study unlike anything that had come before it. Not theoretical projections. Not guesswork about what AI might eventually do. Actual usage data from millions of real conversations with Claude, mapped against the Department of Labor’s occupational database. They called the resulting metric “observed exposure.”

The chart that came out of it is one of the most important visuals in macro analysis right now.

The blue area represents theoretical AI capability...what large language models could do across a given set of job tasks if fully deployed. The red area represents what AI is actually doing right now, based on real professional usage patterns. The gap between the two is the runway still ahead.

Start with the jobs that are largely untouchable. Transport workers: 12.1% theoretical exposure. Agriculture: 15.7%. Construction: 16.9%. Food service: 16.9%. Ground maintenance: 3.9%.

These are jobs that require physical presence and hands-on judgment. Nearly immune to the current displacement wave. As white-collar wages get compressed and these trades become scarcer relative to demand, wages here may actually rise.

Now look at the other end.

Computer and math: 94.3% theoretical exposure. Business and finance: 94.3%. Management: 91.3%. Office and administrative support: 90%. Legal: 89%. Architecture and engineering: 84.8%.

These are the exact occupations that generate the income, the 401(k) contributions, the automatic passive allocations that have been flowing into the S&P 500 for decades.

And Anthropic’s own researchers note that the gap between theoretical capability and observed usage isn’t permanent. Their report is explicit: as capabilities advance and deployment deepens, observed exposure expands toward the theoretical ceiling. The question isn’t whether it gets there. It’s how fast.

The layoff data is already moving in that direction. More than 113,000 tech workers have been cut across 179 distinct layoff events in 2026. That’s an average of 825 job losses per day. 2026 is already running at a pace to rival the record 2023 total.

Meta’s 8,000-person cut, effective May 20, representing roughly 10% of its global workforce, is the single most watched event in that 2026 total. But it isn’t alone. Amazon eliminated 30,000 corporate positions since October 2025, representing roughly 10% of its white-collar workforce. Oracle cut a comparable number in late March. Snap, Cisco, Google: the list grows each week.

What’s different from the 2022–2023 rightsizing cycle is the stated rationale. Pandemic over-hiring was the excuse then. Now, executives are pointing explicitly to AI... and even where that framing is partly cover for routine cost-cutting, it signals where organizational strategy is headed. The intent is to substitute compute for headcount going forward. And that substitution is concentrating in the exact occupational categories that Anthropic’s own data identifies as most exposed.

When Passive Flows Reverse: The S&P 500 Feedback Loop Nobody Is Running

This is where the analysis stops being a trend story and becomes a structural risk story.

During April’s rally, the S&P 500 added roughly $10 trillion in market cap. But market cap figures can be misleading. When a single share trades at a higher price, every other share in that company gets marked to that price, and aggregate market cap jumps by multiples of the actual dollars that changed hands. According to analyst Mike Green’s calculation, something in the range of $400 billion in actual net inflows drove that entire $10 trillion market cap move. Extraordinary leverage between cash in and notional value created.

That leverage is fine when flows are positive. It becomes a serious problem when they reverse.

Baby boomers are retiring at scale. They don’t accumulate passive investments...they draw them down. That’s a structural headwind to passive inflows that was already building before AI entered the picture. Layer on top of it a systematic reduction in white-collar employment and the arithmetic looks very different.

No hiring, no firing...just a slow freeze. That’s been the labor market narrative for most of the last eighteen months. But the AI-driven white-collar displacement now accelerating isn’t a freeze. It’s a directed reduction. And the workers being removed aren’t randomly distributed across the economy. They’re concentrated precisely where passive flows originate.

Think about what that implies for the chain reaction.

Fewer white-collar jobs leads to fewer passive inflows. Fewer inflows weaken the S&P bid. A weaker bid eventually means lower asset prices. Lower asset prices erode consumer confidence. Eroding confidence accelerates hiring freezes. Hiring freezes tip into actual layoffs. And the cycle feeds itself.

A slow-moving train wreck is the right analogy here. Once the train picks up speed going downhill, there’s nothing stopping it...just as there was nothing stopping it going uphill. Thirty years of passive inflows building momentum in one direction has been extraordinary to watch. The same mechanical force working in reverse will be equally powerful. And equally indifferent.

Lower Mortgage Rates and Housing: Why Rate Cuts Won’t Save This Market

The conventional wisdom says: Fed cuts rates, mortgages get cheaper, housing recovers. It sounds reasonable. It’s also the wrong mental model for the current environment.

Higher rates aren’t inherently bad for housing. It depends entirely on why rates are moving. If rates rise because the economy is strong...because wages are rising, inflation is running, aggregate demand is robust... then those higher monthly mortgage payments get absorbed by households whose incomes are also rising. That’s what happened after COVID. That’s why housing prices didn’t collapse despite the most aggressive rate-hiking cycle in decades.

The problem is when rates rise into a weakening economy. Or when rates fall specifically because the economy is collapsing. That’s the 2008 pattern. Oil went to $147. The ECB hiked on July 3, 2008...into an economy already in early-stage crisis. The rate hike made things worse. When rates then fell sharply, that wasn’t a cure. It was a signal that the disease was advanced.

Apply that logic now. If the Fed delivers meaningful, sustained rate cuts in the months ahead, the honest question is: why? Not a hedge-your-bets adjustment in a neutral economy, but real accommodation. That kind of cutting happens when the labor market is deteriorating fast...when credit stress is building... when conditions are deteriorating in ways that make households less willing or able to buy homes regardless of the monthly payment.

Lower rates don’t help housing if the people who would buy a home have been laid off.

Which brings the analysis to the luxury end of the housing market specifically. Toll Brothers, the nation’s leading builder of luxury homes, occupies a telling position in this framework. The company builds primarily for high-income buyers: the affluent professional, the corporate executive, the category of buyer most likely to carry an outsized passive investment account...and also most likely to be among the white-collar workers facing AI-driven employment disruption.

Toll Brothers sits outside the S&P 500. That means it receives no passive bid. No automatic, non-discretionary monthly inflow from America’s payroll cycle props its stock price the way it props S&P components. In a pairs-trade framework, the structure of long SPY / short TOL captures two directional forces simultaneously: long the passive bid that keeps the index supported regardless of fundamentals, short a business that faces headwinds in both rate scenarios (up or down) and whose primary buyer base is the exact cohort most directly exposed to AI-driven job displacement.

This is not a trading recommendation. There are no certainties, only probabilities. But the probabilities align from multiple directions at once... and when that kind of convergence shows up, it’s worth understanding why.

What to Watch

The metric that matters most going forward isn’t the headline jobs number. It’s the composition. How many of the jobs being created are the kind that fund a 401(k) and allocate to an index fund each month? How many of the jobs being lost are in the white-collar categories that Anthropic’s own usage data identifies as most exposed?

The market can sustain a slow reduction in passive inflows for a while. Momentum is real. But once net outflows arrive...pushed by boomer retirements, AI-driven white-collar displacement, and whatever credit event eventually materializes... the same mechanical force that has driven the S&P higher for thirty years works in reverse.

No drama. Just arithmetic.

Facts > Narrative.

Stand up for freedom, liberty, and free market capitalism.

In the 60s, 70s and 80s when there wasn't AI or even much in the way of computers, the major tech companies I worked for could have laid off at least 1/3 of their office employees and saved a lot of money without affecting production. Even back then it was hard to get rid of unproductive people. They would have jumped on the opportunity to lay them off with something like AI as an excuse. I suspect AI is often being used as an excuse. Remember what Musk did when he took over Twitter. He didn't need an excuse to get rid of unproductive people.

This isn't random headcount reduction. Look at the Anthropic data and the pattern is clear: companies are cutting the exact people who fund the 401(k) machine. Engineers, analysts, and finance pros. The high earners.

The second-order hit gets ignored. When a senior dev takes a 30% to 40% pay cut, they don't stop investing, but their contribution shrinks. Multiply that by a few hundred thousand people and you get a massive squeeze on inflows without high unemployment.

The fear isn't about losing a job; it's about the floor dropping. It is a slow squeeze.

The train analogy is right, but most people on board still think the brakes work.