Are Tokenized Deposits the Trojan Horse for Financial Surveillance?

Tokenized deposits promise convenience...but what if they’re the perfect Trojan horse for surveillance and control? Who really owns your money in a tokenized world?

Written by Rebel Capitalist AI. Supervision and Topic Selection by George Gammon

There's a new buzz in the world of finance: tokenized deposits.

JPMorgan has already jumped in with the launch of its own tokenized deposit, JPMD.

To many, these sound like harmless, even helpful innovations.

After all, who wouldn't want faster transactions and more efficient banking systems?

But scratch beneath the surface, and there's a deeper, more concerning story. One that investors and freedom-minded citizens need to pay close attention to.

Tokenized deposits, at their core, are a type of digital representation of regular bank deposits.

They're backed one-to-one by actual cash in a traditional bank account but can move around on a blockchain or digital ledger system.

Sounds good, right? Streamlining transactions, reducing fees, modernizing the old banking infrastructure.

But here’s the catch…what happens when all those tokenized deposits end up on one or two massive ledgers?

And more importantly, what happens when those ledgers aren’t just managed by private institutions, but influenced or outright controlled by the federal government?

The Consolidation of Ledgers: A Hidden Risk

In today's fragmented financial system, privacy still exists in pockets.

Your deposit at a regional bank isn’t immediately visible to your credit card company or your brokerage firm.

Different financial institutions operate with different ledgers, creating natural barriers to full surveillance.

But tokenized deposits could change that.

In an effort to "streamline" finance, we may end up centralizing the entire ecosystem onto just a few mega-ledgers.

Once that happens, it becomes trivial to track, monitor, and control the flow of money.

What does this mean for freedom? For privacy?

It’s the financial equivalent of putting every American’s health records, purchasing habits, location data, and political donations on one giant Google spreadsheet…then handing editing rights to Washington, D.C.

But here’s the kicker…once the financial plumbing gets centralized, it’s not just convenience that improves.

It’s control that concentrates.

And when the architecture is in place, the only question left is: who gets the master key?

Who Controls the Ledger Controls the System

Let’s not forget that we’re living in a world where regulators routinely move into the private sector—and vice versa.

When you have regulators pushing for tokenized deposit infrastructure, then transitioning into the very companies that manage these systems, you get massive conflicts of interest.

This isn’t a theoretical concern. We’ve seen central bankers push for CBDCs (central bank digital currencies) while holding advisory roles at fintech companies.

The same people regulating the infrastructure are often poised to benefit from it.

When the referee starts investing in one of the teams, you should start asking hard questions.

Imagine a world where your financial freedom is contingent not on the Constitution, but on the policies of a few unelected technocrats.

If all tokenized deposits live on a centralized, government-accessible ledger, what happens when the government decides certain behaviors are undesirable?

The revolving door between public regulators and private fintech giants isn’t just a footnote—it’s the blueprint.

And when the same people writing the rules are also writing the code, your rights become a line item in someone else’s profit model.

You Think It Can’t Happen Here? Think Again

We don’t have to look far to see what can go wrong.

In places like China, centralized digital payment platforms are already being used to restrict travel, suppress dissent, and penalize "undesirable" behavior.

Social credit systems sound dystopian—until they’re quietly introduced via modern fintech.

If you think the U.S. is immune, just remember how quickly financial platforms here have frozen accounts or denied service based on political pressure.

Now imagine those platforms are the only game in town—and they all feed into the same ledger.

The infrastructure for financial censorship already exists.

The only thing missing is centralization. And thanks to tokenized deposits, that last puzzle piece is sliding into place right now.

Tokenized Deposits and the Death of Cash?

Tokenized deposits are often sold as a complement to cash, not a replacement.

But ask yourself…why develop this infrastructure unless the goal is to reduce reliance on cash altogether?

Once tokenized systems are in place and made mandatory for certain transactions (say, receiving government aid or paying taxes), it’s only a matter of time before cash becomes functionally obsolete.

Cash is anonymous. It’s permissionless. You don’t need approval from a bank, a regulator, or a tech platform to spend a $20 bill.

Tokenized deposits flip that equation on its head.

Suddenly, your ability to transact could be filtered through algorithms designed by corporations and sanctioned by government bureaucrats.

Once cash becomes impractical, the need for permission will replace the right to privacy.

That’s not a bug in the system…it’s the feature. And the institutions rolling this out?

They’re counting on you not noticing until it’s too late.

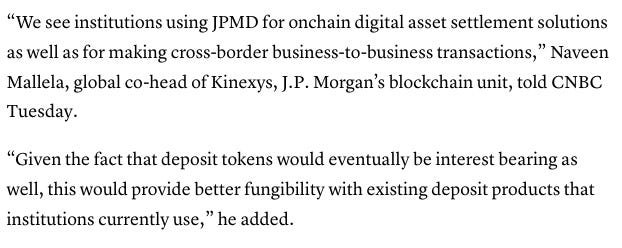

The JPMorgan Token: A Preview of the Future?

One major development that underscores this trend is JPMorgan’s recent launch of its own tokenized deposit called JPMD.

The JPMD token is designed to facilitate large-scale interbank and institutional transactions using blockchain technology, all backed by traditional fiat deposits.

While JPMorgan claims the initiative is about improving speed and transparency, it also shows how quickly the largest banks are moving to dominate this space.

If JPMorgan's ledger becomes a key infrastructure layer, it could set the stage for other banks…or even the government…to piggyback off this control.

What starts as a corporate experiment could soon become the new default for all financial transactions.

JPMorgan’s move isn’t just a step forward in digital finance…it’s a prototype for a new financial regime. One where the rules of access, visibility, and control aren’t up for debate… because they’re embedded in the code.

How Smart Investors Should Be Thinking

For investors, tokenized deposits are both a risk and an opportunity.

The risk lies in assuming this is just a technological upgrade with no downstream consequences.

The opportunity lies in anticipating the consequences before the crowd catches on.

Some smart investors are already positioning in assets that thrive on financial privacy and decentralization…think Bitcoin, precious metals, and certain private equity plays in privacy-focused fintech.

Others are hedging against financial repression by diversifying offshore, acquiring foreign bank accounts, or buying real estate in jurisdictions less susceptible to digital surveillance regimes.

But perhaps the most important move is simply to stay informed.

Understand what tokenized deposits are, what they could become, and who stands to gain from their adoption.

In a world where every transaction could be monitored, filtered, or denied, investing isn’t just about returns…it’s about sovereignty.

The real question is: how do you position yourself before the walls close in?

This Isn't About Tech, It's About Control

The public debate around tokenized deposits often focuses on technical issues: latency, throughput, regulatory clarity.

But the real debate is about values.

Do we want a financial system that prioritizes freedom and decentralization, or one that enables surveillance and control?

Don’t be distracted by buzzwords. Blockchain is not inherently liberating.

Tokenization is not inherently democratic. It all comes down to who controls the ledger.

Because once that control is lost, getting it back may be impossible.

This Friday, George Gammon is hosting his first live Q&A exclusively for paid subscribers.

It’s your chance to ask questions, get real-time macro insight, and hear George’s unfiltered take on what’s really happening behind the headlines.

Plus, we’re releasing a subscriber-only explainer video on how Quantitative Easing actually works…not the textbook version, but the real mechanics they never teach you in school.

If you want to understand how money is really created, and how it’s quietly reshaping the world around you, this video is essential.

Join the thousands of liberty-minded investors who already trust the Rebel Capitalist News Desk for macro insight you won’t find anywhere else.

Upgrade to paid now and get immediate access to all upcoming Q&As, George’s private video briefings, and everything else we don’t publish publicly.

Rebel Capitalist AI

Supervision and Topic Selection by George Gammon

June 17, 2025