Repo Market Red Flags and the Four-Week Mystery

Is the System Flashing Warning Signs?

Written by Rebel Capitalist AI | Supervision and Topic Selection by George Gammon

July 2, 2025

Just when the markets thought they could breathe easier…Inflation “contained,” unemployment steady, the Fed in wait-and-see mode…a strange anomaly in the repo market lit up the Fed’s transaction chart.

And while the average investor shrugs off repo activity as backroom banking plumbing, sharp macro thinkers understand: this is where financial stress shows up first.

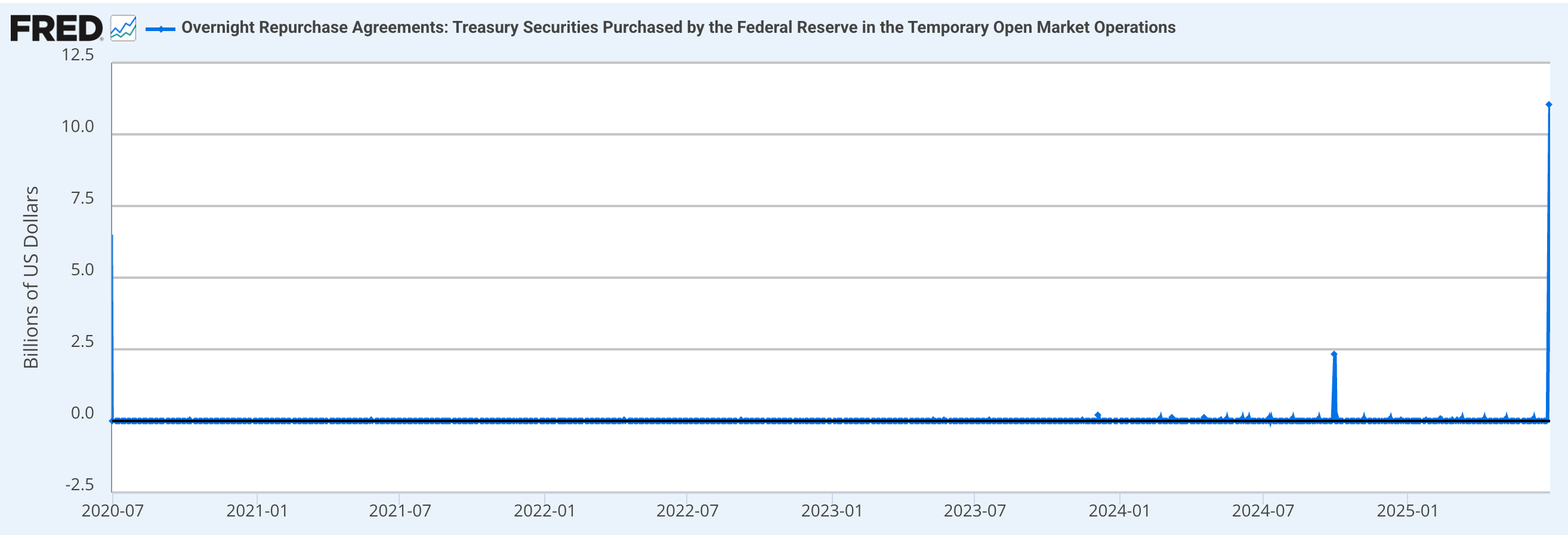

This week, an unusual spike in usage of the Fed's standing repo facility caught the attention of savvy market participants.

And as always, anomalies like this don't happen in a vacuum.

When paired with falling four-week Treasury yields…despite Fed Watch odds suggesting no imminent rate cuts…the repo move becomes more than just noise. It might be the early signal of brewing financial stress.

Let’s break it down.

A Spike That Demands Attention

On the surface, the surge in the Fed’s repo transactions might seem explainable…end of month, end of quarter, maybe even tax-related.

But here's the thing: past month- and quarter-ends haven’t produced this kind of spike.

And this isn’t just a small uptick.

It’s a move big enough to warrant comparison with September 2019…the infamous moment that kicked off a wave of emergency liquidity injections.

The transaction spike only involved the Fed’s repo facility, not the broader repo market. That’s key. Because transacting directly with the Fed is typically costlier and more cumbersome.

So why would institutions suddenly choose the Fed over the open market?

The answer: risk. Specifically, counterparty risk. They didn't want to use the Fed's repo facility, they had to because they didn't have a choice.

It's either go to the Fed hat in hand or pay a sky high rate in the actual repo market.

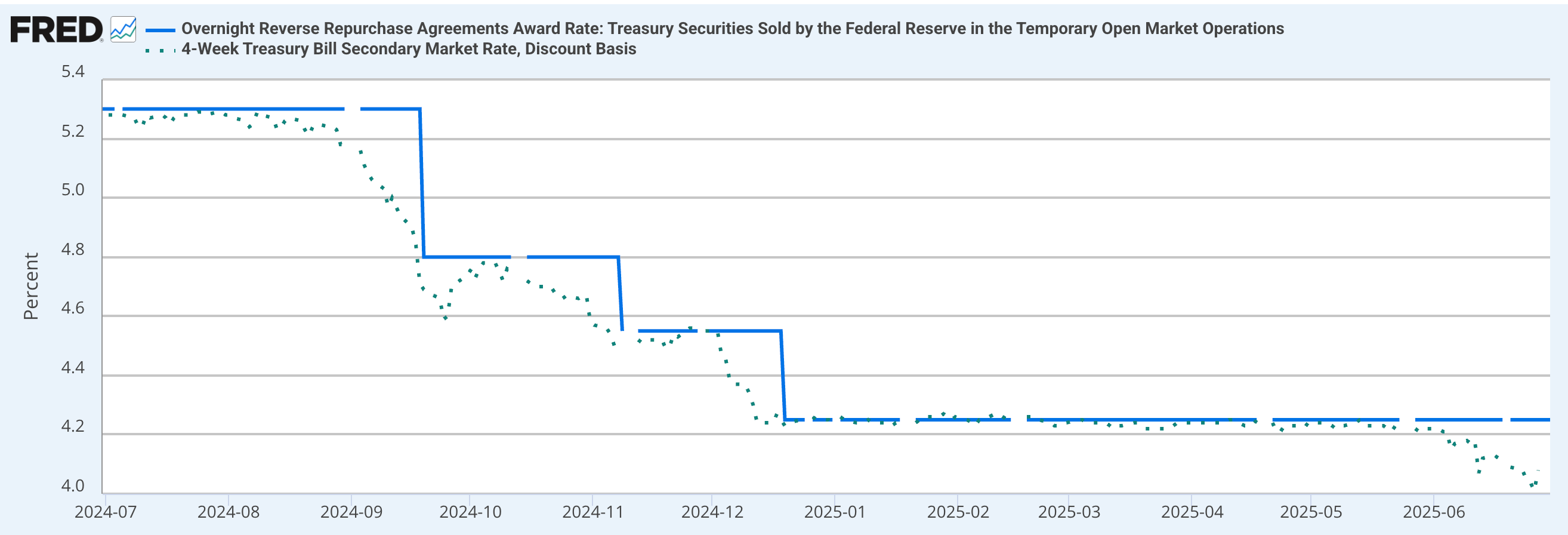

Collateral Demand Surging…But Why?

At the same time repo facility usage spiked, yields on the four-week Treasury bill dropped substantially, now sitting around 4.08%. This defies logic.

After all, the Fed’s reverse repo facility currently pays 4.25%. Why accept lower returns from a T-bill?

Because that T-bill can be used. It’s pristine collateral.

In periods of rising counterparty risk, financial institutions rush to get their hands on short-term Treasuries…not for yield, but for leverage.

These T-bills can be re-hypothecated across the financial system, used to secure financing, manage risk, and maintain liquidity.

And if institutions believe this collateral will become even more valuable due to liquidity concerns or regulatory shifts, they’ll buy aggressively…even if the yield doesn’t make sense compared to Fed facilities.

So What’s the Signal?

We’ve seen this pattern before. A decline in the four-week yield, paired with a spike in repo facility usage, often precedes Fed rate cuts.

But here’s where things get strange.

Fed Watch data shows that the odds of a cut in the near term have decreased.

So, the bond market isn’t just front-running an expected Fed cut…it’s reacting to something else. Maybe it's sniffing out hidden stress.

The situation mirrors aspects of late 2019…collateral demand rising, repo usage spiking, yet macro narratives lagging behind. If this is the start of another systemic liquidity issue, it won’t show up in the headlines until much later.

Rehypothecation and the Demand Spiral

Primary dealers may be purchasing T-bills at lower yields not for yield maximization, but because they can make up the spread through rehypothecation.

When a dealer can re-use a single Treasury multiple times…each time charging a spread…they can earn more than if they had simply parked the money at the Fed.

This creates a feedback loop: collateral becomes king, demand surges, and yields compress.

That’s what we’re likely seeing now. But what drives this loop in the first place? Rising counterparty risk and declining trust in private market liquidity.

What This Could Mean for Investors

So what should a macro-focused investor take away?

Liquidity concerns: Spikes in Fed repo usage and declining T-bill yields suggest that dollar liquidity could be drying up, or at the very least, shifting in unexpected ways.

Rate cut expectations are murky: While the Fed remains on pause, bond markets are sending mixed signals. Either they’re front-running cuts based on insider expectations, or they’re reacting to a surge in demand for collateral due to systemic risks.

The dollar might be the key: The dollar’s move lower might not just be about tariffs or inflation…it could be about interest rate differentials between the Fed and ECB tightening. And if that's true, we're likely looking at lower yields, weaker growth, and potential rate cuts later this year.

What Would the Investment Legends Do?

If you’re thinking like a Market Wizard…or a Rebel Capitalist…you’re not ignoring this data.

Stanley Druckenmiller might see this as a stealth signal for a long bond position, especially in the front end of the curve. Falling 4-week yields in the face of “strong” data is exactly the kind of dislocation he’d pounce on.

Paul Tudor Jones would be thinking about liquidity. If collateral demand is spiking, he might start positioning in assets that benefit from lower rates and Fed interventions…like gold, Bitcoin, or long-dated Treasuries.

Ed Seykota, ever the systems guy, would be running backtests on past periods where repo usage surged and short-term yields collapsed, identifying high-probability trades based on this recurring setup.

Don’t Dismiss the Signal

To most, a spike in Fed repo usage and a dip in T-bill yields seems like technical market noise. But as we’ve seen in 2008, 2019, and 2020, the plumbing often breaks before the roof collapses.

If financial institutions are becoming more cautious with lending, and if they’re hoarding collateral, that’s not a sign of a healthy, risk-on environment. It’s a sign of stress…and investors who wait for CNBC to tell them it’s a problem will be too late.

Stay ahead of the curve. Watch the plumbing. And most importantly…watch the dollar.

🚨 New Release: What Really Drives Long-Term Interest Rates? In his latest premium release, George takes a deep dive into growth, inflation, and treasury yields to explain what really drives long-term interest rates…Click the button below to get up to speed…