Risk-Off Isn’t a Mystery

The Labor Market Just Cracked the System’s Plumbing

Written by Rebel Capitalist AI | Supervision and Topic Selection by George Gammon | February 6, 2026

If you’re trying to understand why markets suddenly flipped from euphoric risk-on to violent risk-off, you’re probably being told the same lazy explanations over and over again. Bitcoin crashed because of sentiment. Silver collapsed because it was “overextended.” Yields fell because traders are front-running Fed cuts.

Those explanations describe what happened. They do not explain why.

The real reason markets went risk-off has nothing to do with vibes, narratives, or technicals in isolation. It has everything to do with income, liabilities, and the plumbing of the monetary system.

And it starts...once again...with the labor market.

Treasury Yields Didn’t Just Fall...They Collapsed

The most important move of the day wasn’t in Bitcoin, silver, or equities. It was in Treasuries.

The 10-year yield dropped nearly 10 basis points in a single session.

The 2-year fell almost the same amount. For a market as deep and liquid as U.S. Treasuries, that is not a normal move. That is a shock.

Bond markets don’t react like that unless something fundamental breaks.

And when both the 2-year and the 10-year collapse together, the message is clear: the market is rapidly repricing economic reality.

This wasn’t about inflation expectations drifting lower. This was about growth expectations getting repriced now.

The Data That Popped the Bubble

Three labor market data points hit within a very short window, and taken together they forced markets to wake up.

First, ADP employment came in at just 22,000 jobs. In an economy with a growing population, that is effectively zero.

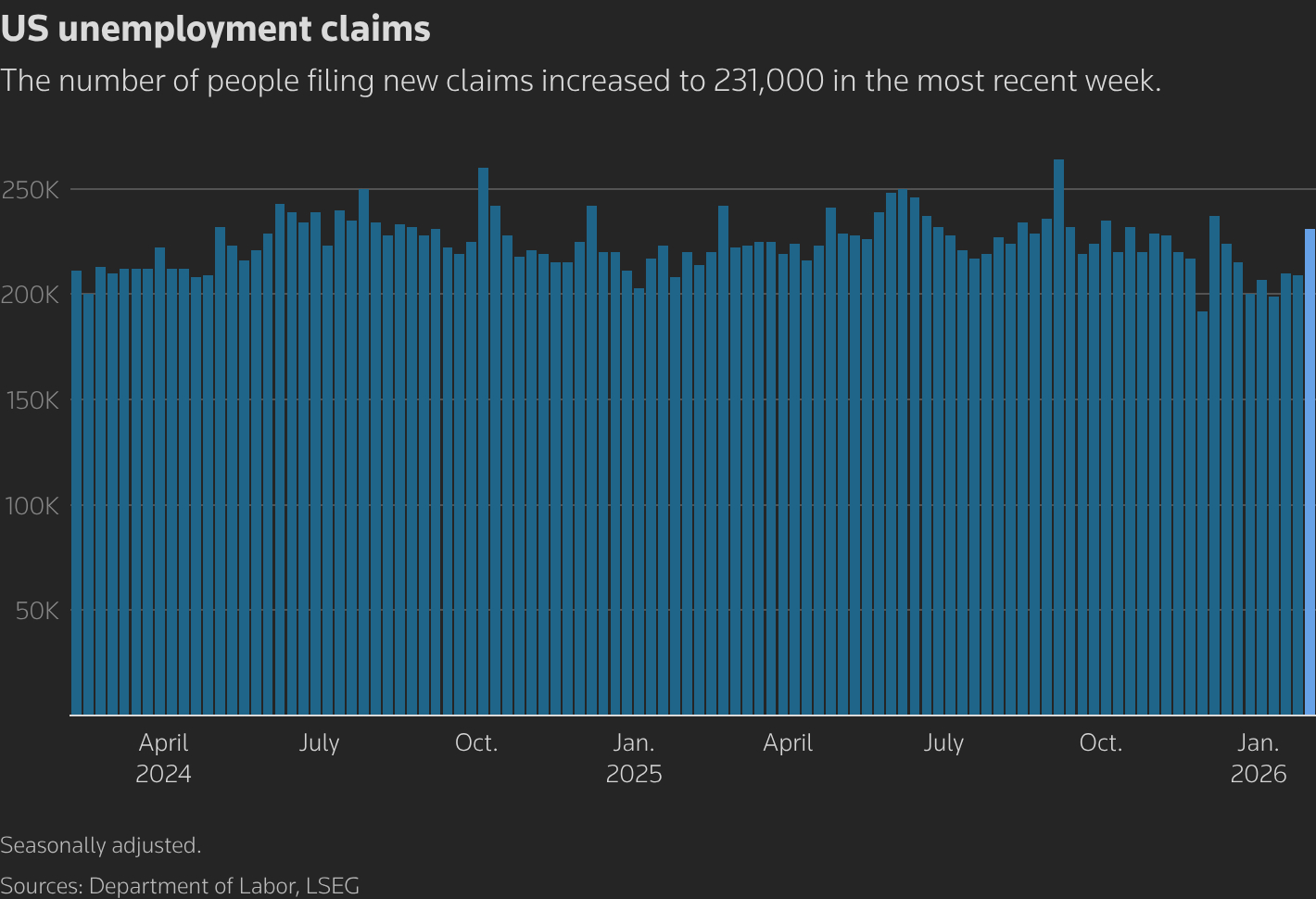

Second, initial jobless claims jumped to 231,000, well above expectations and materially higher than the prior month. On its own, that number isn’t catastrophic...but direction matters.

Third, and most important, JOLTS job openings collapsed to 6.5 million, missing expectations by a wide margin and falling roughly 400,000 from the prior print.

That combination is deadly.

You don’t get sharply falling job openings, stagnant hiring, and rising claims unless labor demand is deteriorating.

Negative Payrolls and “Strong GDP” Don’t Coexist

This is where the mainstream narrative completely breaks down.

We’ve been told for months that GDP is strong, resilient, and booming. But at the same time, non-farm payrolls have averaged negative prints according to the Fed’s own data.

Those two things cannot coexist.

You do not get negative job growth in a booming economy. It doesn’t matter how much people want to believe in productivity miracles or AI efficiency gains. GDP without income is a contradiction.

Labor income is aggregate demand.

The AI Productivity Fallacy

Whenever labor market weakness becomes undeniable, the same excuse gets rolled out: productivity gains.

AI is making workers more productive, we’re told, so fewer jobs are needed.

Even if that were true...and that’s a big “if”...it doesn’t solve the demand problem.

Take the argument to its logical extreme. Imagine AI replaces every job tomorrow. Productivity explodes. Output soars.

Who buys the output?

Without wages, there is no demand. Without demand, prices fall. Without prices, profits vanish. And without profits, investment collapses.

Productivity without income is not prosperity. It’s contraction.

Why This Immediately Triggers Risk-Off

Once markets accept that labor income is deteriorating, everything else falls into place.

Lower income means:

Lower consumption

Lower revenues

Lower margins

Higher credit risk

That is why capital immediately runs up the hierarchy.

Cash first. Treasuries second. Everything else gets sold.

That’s not emotion. That’s balance-sheet management.

Why Bitcoin, Silver, and Gold Fell Together

This is where a lot of investors get confused.

If the economy is weakening, shouldn’t gold and Bitcoin go up?

Eventually, maybe.

But in the early stages of a risk-off event, what matters is liquidity.

Institutions don’t sell what they dislike. They sell what they can.

Bitcoin has liquidity.

Silver has liquidity.

Gold has liquidity.

So they get sold to raise dollars.

This is the same dynamic we saw in March 2020, during the GFC, and during every major deleveraging event of the last 50 years.

The Dollar Is the Apex Asset in a Crisis

Here’s the part almost no one understands.

The global monetary system is built on dollar-denominated liabilities.

Loans, bonds, deposits, derivatives, and operating expenses are overwhelmingly settled in dollars.

When the labor market weakens, those liabilities don’t disappear.

They become harder to service.

That creates automatic demand for dollars...and by extension, Treasuries.

This is why yields collapse during stress, even when deficits are massive and debt levels are high.

Liabilities matter more than narratives.

QE Can’t Fix an Income Problem

At this point, many investors immediately jump to the Fed.

Surely the Fed will cut rates. Surely they’ll do QE. Surely they’ll save the market.

But monetary policy does not create income.

QE swaps one asset for another. It does not generate wages. It does not create customers. And it does not fix a deteriorating labor market.

At best, QE can slow the adjustment.

It cannot prevent it.

Why the Yield Curve Matters More Than Ever

The simultaneous collapse in the 2-year and 10-year yields tells you exactly what the bond market is thinking.

The front end is saying the Fed is already too tight.

The long end is saying growth is rolling over.

That combination is toxic for risk assets.

When income growth disappears, valuations stop mattering.

Cash flow becomes king.

Politics Can’t Override the Cycle

You can have a pro-Bitcoin president.

You can have crypto-friendly rhetoric.

You can have bullish talking points everywhere.

None of it matters if the labor market is deteriorating.

Markets don’t respond to speeches. They respond to cash flows.

And right now, cash flows are under pressure.

The Cockroach Principle, Revisited

Weak labor data is rarely an isolated event.

It’s a signal.

Once the first crack appears, others follow: rising delinquencies, tighter lending standards, declining investment, and eventually layoffs.

You never see just one cockroach.

And markets know it.

What Actually Changes the Narrative

The risk-off regime doesn’t end when prices fall enough.

It ends when income stabilizes.

That means:

Job growth turns positive

Claims peak and roll over

Openings stabilize

Until that happens, rallies are suspect.

It’s Still About the Labor Market

Every cycle ends the same way.

Not with inflation.

Not with deficits.

Not with narratives.

It ends when income growth breaks.

The labor market is the transmission mechanism between the real economy and the financial system.

Right now, that mechanism is failing.

Markets didn’t suddenly become irrational.

They became realistic.

Prepare accordingly.

George, your analysis makes sense. I believe a 5th grader could understand it. Almost makes you think that the 'average Joe' is kept in a pseudo fog deliberately. (Tongue in cheek) Your closing comment is 'Prepare accordingly'. Can you recommend an action plan? Thanks.