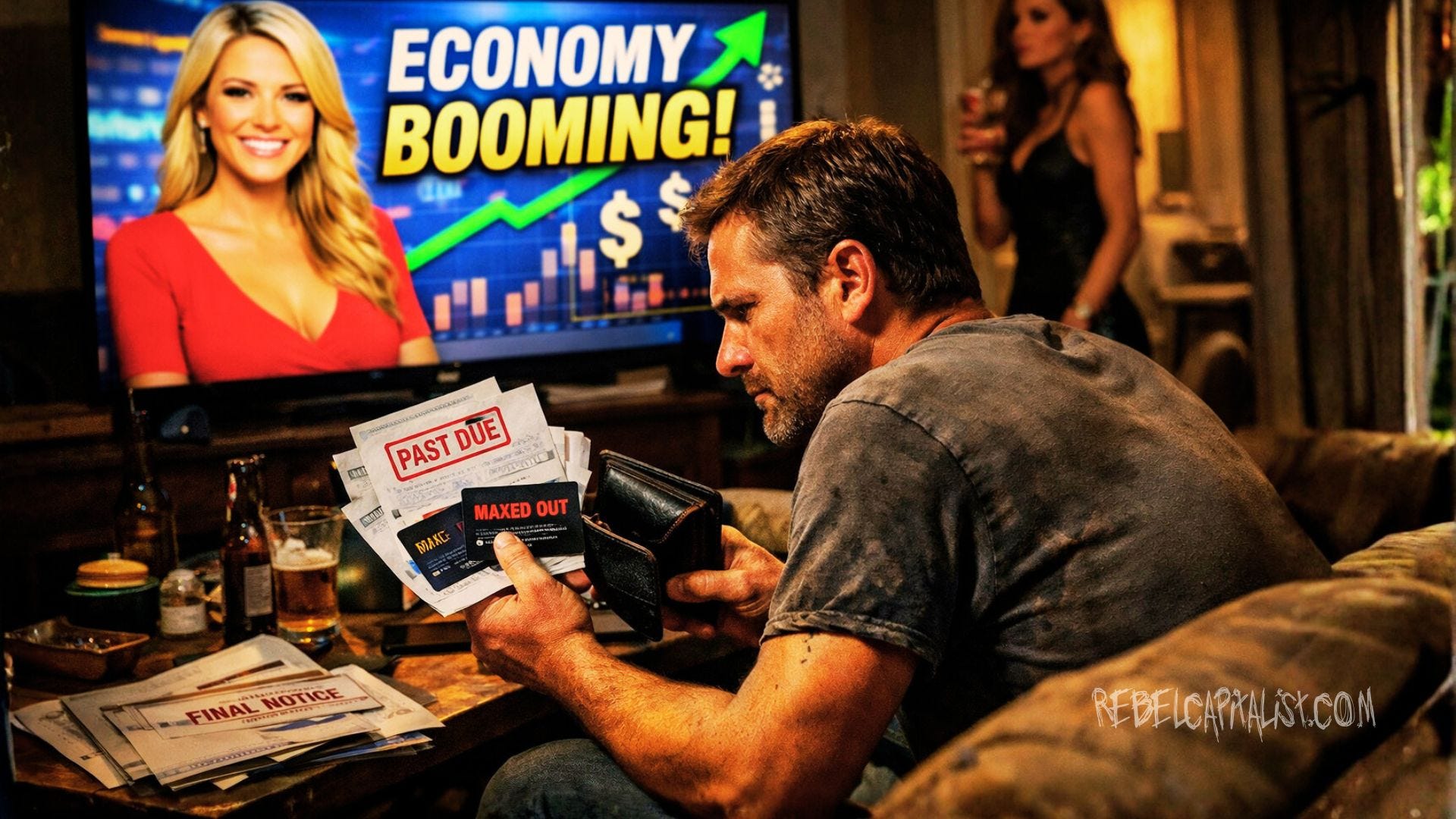

The “Boom Session” Lie

When GDP Gaslights 90% of America

Written by Rebel Capitalist AI | Supervision and Topic Selection by George Gammon | February 19, 2026

Apparently, we’re in a boom.

Not just any boom.

A boom so strong that if you feel broke, stressed, unable to find a good job, or worried about rent…you’re just imagining it.

That’s the new narrative.

According to the latest mainstream analysis, the economy is growing nicely. GDP is solid. The stock market is strong. Consumers are “spending big.” And if you feel like you’re falling behind, that’s a vibe problem…not a data problem .

They even have a name for it now:

The “boom session.”

Translation: The economy is booming, but people are just too negative to realize it.

Let’s break down why that narrative isn’t just wrong…it’s economically incoherent.

The Entire Argument Rests on One Data Point

When you dig into the analysis, something becomes immediately obvious.

The boom narrative is built almost entirely on one metric:

GDP growth.

That’s it.

GDP is positive, therefore the economy is strong. End of discussion.

But here’s the problem.

GDP is an aggregate statistic. It does not tell you:

Who is spending.

Who is earning.

Who is struggling.

Whether labor income is rising.

Whether purchasing power is improving.

It simply measures total output.

And when 60% of Americans believe the country is in a recession, you have to ask a basic question:

Is the public delusional?

Or is GDP incomplete?

Retail Sales Don’t Scream “Boom”

If consumers are “spending big,” the data should reflect it.

Retail sales recently printed 0% month-over-month .

Zero.

And that’s before adjusting for inflation.

Real retail sales, therefore, were negative.

Does that sound like a consumption boom?

Or does that sound like a household sector under pressure?

If aggregate demand were truly surging across the population, we wouldn’t see stagnation in real retail sales.

We would see acceleration.

The Labor Market Contradiction

We’re also told the economy is strong…yet:

Job openings have fallen to their lowest levels since 2020.

Layoffs surged more than 200% from December to January, according to Challenger data.

Major corporations like Nike, Amazon, and UPS have announced large-scale job cuts.

And yet this is framed as a “jobless boom.”

That phrase alone should make you pause.

A boom requires income growth.

Income growth requires jobs.

If hiring is slowing and layoffs are accelerating, aggregate demand eventually follows.

You cannot have a sustainable boom while employment momentum deteriorates.

That’s not ideology.

That’s arithmetic.

Consumer Sentiment Is at Historic Lows…During “Strong” GDP

One of the most striking charts highlighted in the discussion compares GDP growth to consumer sentiment going back to the 1960s.

Historically, when GDP growth was strong…say 4% to 6%…consumer confidence was high.

But today?

GDP growth is reported north of 4%…yet consumer sentiment sits near historic lows.

That divergence has almost never occurred before.

The mainstream interpretation?

Consumers are irrational.

A more grounded interpretation?

GDP may not be reflecting the lived economic reality of most households.

The Distribution Problem No One Wants to Admit

Here’s the uncomfortable truth.

Higher-income households disproportionately own:

Stocks

Real estate

Financial assets

When asset prices rise, the top 10% benefit massively.

Meanwhile, lower-income households spend a far larger percentage of their income on:

Rent

Food

Utilities

Insurance

Healthcare

If inflation in necessities outpaces wage growth, their real standard of living declines…even if GDP is rising.

That creates a K-shaped dynamic.

Aggregate output can grow.

Asset markets can surge.

And yet the majority of households can feel worse off.

That’s not a vibe.

That’s distribution.

Productivity Gains and the AI Illusion

Another bullish talking point is surging productivity.

Output per worker has hit all-time highs.

Much of that is attributed to AI.

But here’s the overlooked dynamic:

Productivity gains that reduce headcount may boost margins…but they also reduce aggregate wage income.

If companies increase output while cutting jobs, total supply increases.

But total demand can stagnate…or fall…if displaced workers lose income.

In the short term, that’s disinflationary.

And if layoffs accelerate…as the data suggests…that’s not a boom.

That’s tightening labor conditions.

“Jobless Boom” Is an Oxymoron

Economists describing this as a “jobless boom” are inadvertently highlighting the contradiction.

If GDP growth does not translate into job growth, then the benefits of that growth are not broad-based.

If the benefits are not broad-based, consumer confidence collapses.

If consumer confidence collapses, spending eventually slows.

And if spending slows, GDP slows.

You can mask that dynamic temporarily with:

Asset-price wealth effects

Fiscal deficits

Inventory accumulation

But you cannot override the income channel indefinitely.

The Asset Market Backstop Is Fragile

One counterargument is that the top 10% can spend enough to sustain growth.

In theory, high-income households can offset weakness elsewhere.

But that thesis relies on a key assumption:

That asset prices remain elevated.

If the S&P 500 were to fall 30% and stay there, what happens?

Wealth effects reverse.

Confidence weakens.

Spending contracts.

The very mechanism propping up aggregate demand becomes the transmission channel for contraction.

That’s why relying on asset markets to justify broad economic strength is dangerous.

It works…until it doesn’t.

60% of Americans Think We’re in a Recession

Let’s come back to that number.

Nearly three-fifths of Americans believe the U.S. is currently in a recession.

That is not a marginal misperception.

That is a supermajority.

If 60% of households feel recessionary pressure, that means:

Income growth is insufficient.

Purchasing power has eroded.

Financial stability feels fragile.

You cannot dismiss that as “bad vibes.”

Consumer psychology is a leading indicator.

When households feel unstable, they cut discretionary spending.

When discretionary spending falls, GDP follows.

GDP Can Rise While Living Standards Fall

Here’s the macro nuance.

GDP measures production.

It does not measure:

Distribution of gains.

Real purchasing power.

Household balance-sheet stress.

Financial fragility.

You can have positive GDP growth fueled by:

Government deficit spending.

Corporate margin expansion.

Productivity gains.

Asset-price appreciation.

While median real wages stagnate.

That combination produces exactly what we’re seeing:

Strong headline GDP.

Weak consumer sentiment.

Slowing labor demand.

Rising layoffs.

Stagnant retail sales.

That’s not a boom.

That’s imbalance.

The Real Risk: Narrative Overconfidence

The most dangerous aspect of the “boom session” narrative isn’t that it’s optimistic.

It’s that it dismisses warning signs.

When you ignore:

Declining job openings.

Surging layoffs.

Weak real retail sales.

Collapsing consumer sentiment.

You miss inflection points.

And macro cycles turn at inflection points.

Not when everyone agrees.

Final Thought: Data vs. Experience

There’s a difference between:

“GDP is growing.”

And:

“Living standards are improving.”

If a majority of Americans feel financially unstable, that signal deserves investigation…not dismissal.

GDP can be revised.

Sentiment can deteriorate.

Asset markets can correct.

But household cash flow constraints are real.

You cannot gaslight aggregate demand.

Eventually, it shows up in the numbers.

The real question isn’t whether GDP is positive.

It’s whether income growth is broad enough to sustain it.

Right now, the divergence between headline growth and household reality suggests something is off.

And when divergences persist in macroeconomics, they rarely resolve upward.

Prepare accordingly.

https://fred.stlouisfed.org/series/RETAILSMNSA

This chart I found only goes up to November of last year. But one can see it has *exactly* the same pattern *every year*. It goes up every month, or some months two months in a row, and down the next month or two; the same month or two months in the same way, same relative degree as the year before, year after year. The only differences are in scale of the pattern, but the pattern is the main; and secondly, that the height always goes up and up year after year (but in PPP against the past, probably not, yes?).

So what about February. Every single year, it is the very bottom of the year's chief dip, the after the Christmas sales cliff drop...