The Dollar Crashes Up. Not Down.

US dollar swap lines are back...and every pundit is screaming bond market blowup. The data says the exact opposite. Here’s what the real signal means.

![[Section Divider Image]](https://substackcdn.com/image/fetch/$s_!wdAh!,f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F6937714b-9b1a-4408-8c84-27a8472c6573_1320x50.webp "[Section Divider Image]")

Every pundit with a social media account has had the same take this month. Scott Bessent’s public defense of US dollar swap lines with Gulf states and Asian allies? Bond market blowup. The debt crisis finally arriving at the front door. Treasury yields through the roof while the dollar implodes. The Fed and the Treasury are propping up a system on the verge of collapse, and the swap lines are the smoking gun.

Come on, now.

That narrative has exactly one thing going for it: it sounds compelling. But once the actual mechanics get unpacked, the story runs almost perfectly backwards. It’s precisely because the dollar is so structurally irreplaceable that every major oil-importing economy on the planet is standing in line asking for one.

The real signal buried inside this story is profoundly uncomfortable for anyone who has spent the last three years positioned for the dollar to roll over.

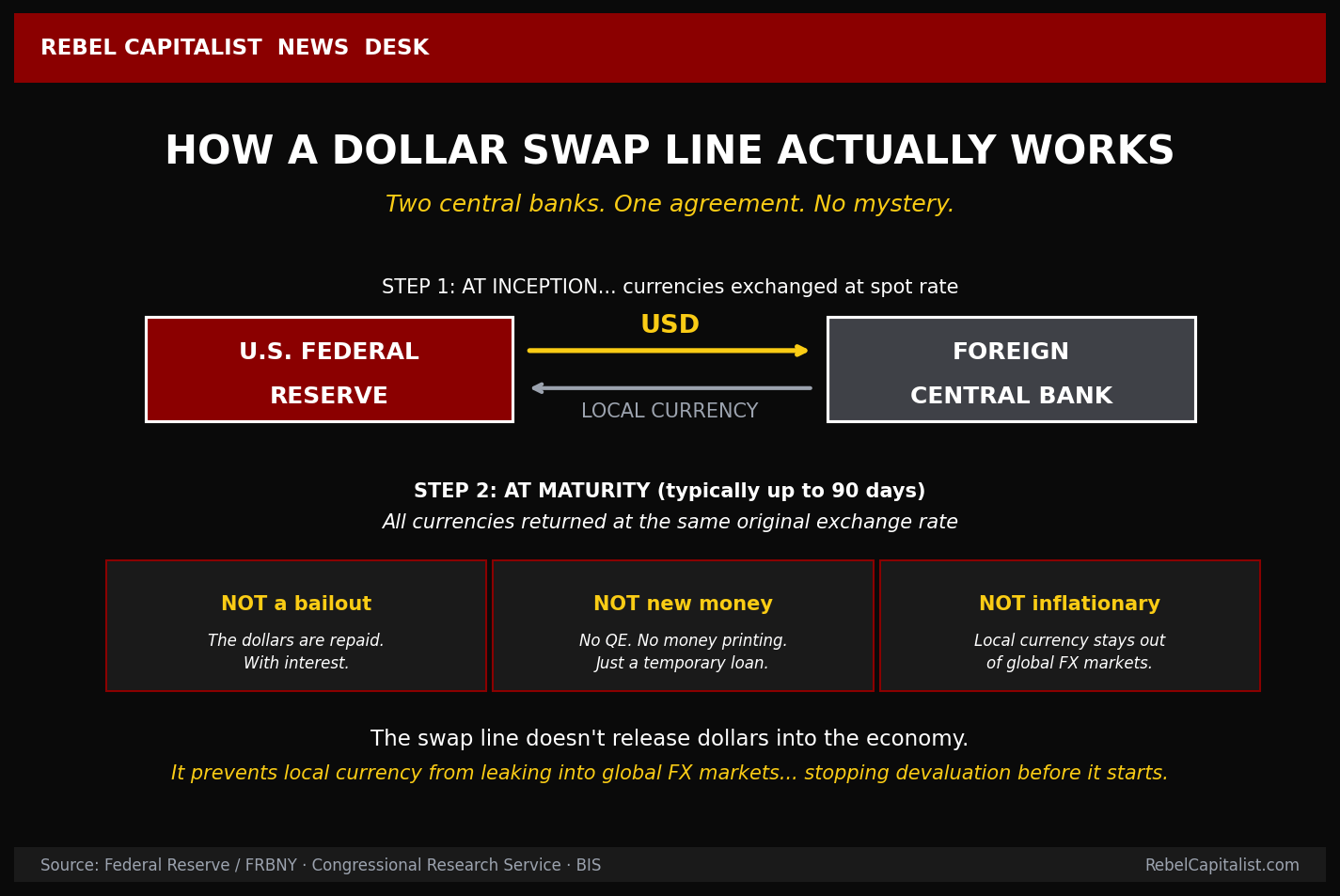

What a Dollar Swap Line Is (And What It Isn’t)

The mechanics are simple enough that the hysteria surrounding US dollar swap lines becomes immediately puzzling once you actually understand them.

Two central banks. One agreement. The Federal Reserve deposits dollars into a foreign central bank’s account. That central bank deposits an equivalent amount of its own currency into the Fed’s account. At a specified future date...typically within 90 days...the transaction reverses. Both parties get their original currency back, and the Fed collects a modest interest payment.

That’s it.

Think of it as a repo transaction but instead of using Treasuries and dollars as the two legs, you’re using dollars and a foreign currency. The Fed has operated these arrangements since the early 1960s, deploying them during the 2008 Global Financial Crisis and reactivating them for COVID in March 2020.

What a swap line is not: a bailout in the traditional sense. The dollars are always returned. No new dollars enter the broader economy. No quantitative easing. No money printing. The cash goes from the Fed to a foreign central bank and stays on institutional balance sheets until the reversal. The foreign currency that flows the other direction just sits in the Fed’s account collecting interest...largely inert.

Why Japan and the UAE Are Lining Up for Dollars

So why is everyone suddenly asking for one?

The Iran war and the effective closure of the Strait of Hormuz created a dollar-funding crunch that cuts to the core of how oil-importing economies function. Japan imports roughly 95% of its oil from the Middle East, with around 70% transiting the Strait. When that route effectively closed, the dollar cost of securing oil intensified. Japanese corporations need dollars to buy oil, and when those dollars aren’t available through normal channels, they have to get them somewhere.

Here’s where the FX mechanics matter.

If a Japanese corporation can’t get dollars from its central bank, it goes to the foreign exchange market. It sells yen, buys dollars, and uses those dollars to purchase the oil it needs. The problem: every yen sold outside Japan puts additional downward pressure on the yen in global FX markets. More yen circulating globally, more demand for dollars, yen depreciates further. The BOJ has been intervening to defend the critical 160 yen-per-dollar threshold... literally spending dollar reserves to stop its own currency from collapsing... and this is precisely the dynamic a swap line short-circuits.

When the central bank has the dollars sitting in its own account, the corporation can get what it needs without touching global FX at all. The yen stays contained. No spillover.

The UAE situation follows the same logic with one additional wrinkle. The dirham has been pegged to the US dollar since 1997 at a fixed rate of 3.6725 AED per USD. That peg is a cornerstone of UAE monetary policy. Maintaining it requires a stable, reliable supply of dollars. When Strait of Hormuz disruptions cut off oil revenue while simultaneously raising dollar demand, the UAE Central Bank governor flew to Washington. Not because the UAE is in financial distress... the country holds roughly $285 billion in foreign reserves...but because the nature of the stress is liquidity, not solvency. A swap line is insurance against the dollar crunch that peg defense requires.

Gulf allies and Asian partners requested the arrangements as backstops. Bessent framed that as proof of dollar primacy. He’s right in the narrow sense. Where the framing gets promotional is in implying the US is doing these countries a favor by keeping them loyal to the dollar. The truth is more blunt: they don’t have a realistic alternative. Not because they haven’t considered it... but because no other currency comes close to the dollar’s network effect. Until something arrives that isn’t just marginally better but exponentially better, countries aren’t walking away. Swap line or no swap line.

So if every major oil-importing economy is standing in line asking for dollar access... while simultaneously burning reserves to defend their own currencies against dollar scarcity... what does that tell you about the direction the dollar is actually heading?