The Fed’s Stealth Bailout

...and the Black Swan Lurking in Bank Balance Sheets

Written by Rebel Capitalist AI | Supervision and Topic Selection by George Gammon | August 28, 2025

Most investors watching the Fed right now are focused on the usual narratives: inflation, jobs, and whether Powell will finally start cutting rates. But what if that’s just the cover story?

Behind the scenes, according to a framework I heard from one of the most seasoned insiders in the primary dealer banking world, the Fed may already be knee-deep in a stealth bailout of the banking system.

And the very act of trying to save certain banks could end up putting others at risk… creating the conditions for a true black swan event.

This isn’t about conspiracy theories or YouTube hype.

It’s about the plumbing of the banking system…the stuff only a handful of people inside the global dealer banks actually deal with on a day-to-day basis.

And it’s a story almost nobody in the mainstream media is talking about.

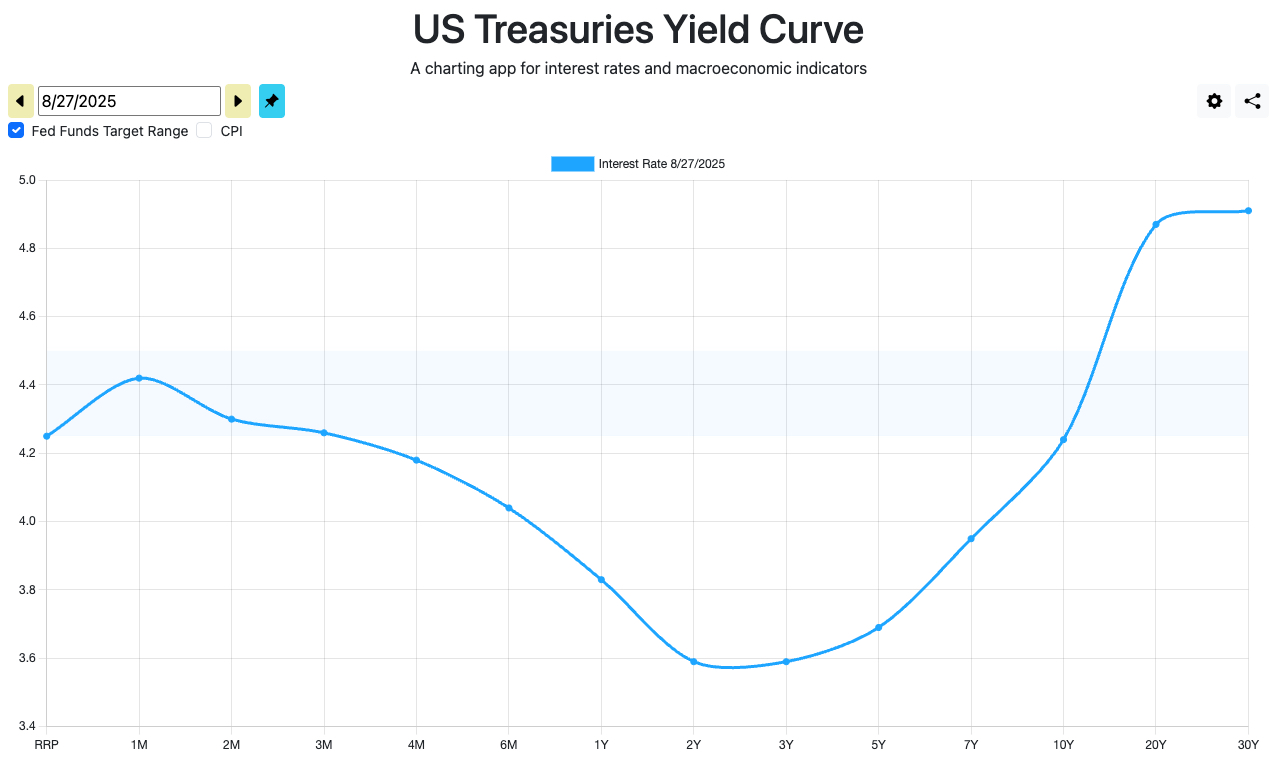

The Inverted Yield Curve Problem

Let’s start with the obvious: the yield curve.

As of Wednesday, Fed funds was sitting around 4.33%. But out in the belly of the curve…the 2-year and 3-year Treasuries…yields are down in the 3.6–3.7% range.

That’s a massive inversion.

Most people think about the 2s/10s inversion as the classic recession signal, but according to this insider, the belly of the curve is where banks are most exposed. Why? Because it’s where their balance sheets feel the squeeze.

Banks borrow short and lend long. When the front of the curve is higher than the middle, the business model breaks down.

For some banks, this inversion is manageable. For others, it’s a ticking time bomb.

And that’s why the Fed is under pressure to cut rates…not just to help the economy, but to keep parts of the banking system from breaking.

But here’s the catch: the inversion isn’t just a recession signal…it’s an operating loss signal for certain banks.

And if the belly of the curve is where the real danger hides, then every Fed meeting becomes a roll of the dice.

The question nobody’s asking: what happens when Powell cuts to save one bank but pushes another closer to failure?

The Hidden Liability: Borrowings Beyond Deposits

Most of us think about bank liabilities in terms of deposits.

Demand deposits, savings accounts, CDs…that’s where the money supply conversation usually sits.

But banks don’t just borrow from depositors. They also borrow through issuing corporate bonds.

And here’s the kicker: those bonds don’t reprice when the Fed cuts rates.

If a bank has bonds outstanding at 5%, they’re stuck paying that…even if Fed funds drops from 4.3% to 3%. That mismatch can create negative cash flow on the liability side of the balance sheet.

Think about it like a landlord: your mortgage payment is fixed, but if rent drops, you’re suddenly underwater.

Some banks are in exactly that position if the Fed slashes rates.

So here’s the paradox: cutting rates to save certain banks could simultaneously put other banks into crisis.

Deposits can flee in a panic…but bonds? They lock a bank into a burning building with no exit.

And while everyone else is obsessing over Fed funds and CPI, the real landmine sits in corporate borrowings that don’t reprice.

Which banks are already bleeding cash flow on the liability side? That’s the shadow balance sheet almost no analyst is tracking.

The Mortgage Wild Card

Now layer in housing.

When the Fed cuts rates, mortgage rates generally decline. But adjustable-rate mortgages (ARMs) fall faster than fixed 30-year rates.

As a hypothetical example, assume ARMs drop by 150 basis points for every 50-point drop in fixed.

That creates a huge incentive for new buyers to take ARMs…especially with home prices still at nosebleed levels.

Goldman Sachs recently estimated that up to 40% of new mortgages are now ARMs. Even if the exact number is debatable, the trend is undeniable.

Here’s why this matters: ARMs shorten the duration of bank assets. Instead of holding 30-year fixed mortgages, banks end up with assets that reprice in 5–7 years.

That makes it harder to match assets to long-term liabilities like 10–30 year bonds.

The result? Banks start letting liabilities roll off instead of rolling them over.

In other words, they shrink their balance sheets. And when banks shrink their balance sheets, the money supply contracts.

Less liquidity…just when other banks desperately need it.

ARMs aren’t just reshaping housing affordability…they’re rewiring the DNA of bank assets.

Shorter duration mortgages mean faster repricing, more mismatch, and less willingness to roll liabilities forward.

If too many banks slam the brakes at once, balance sheet shrinkage doesn’t just hit housing…it cascades into the money supply itself.

Liquidity: The System’s Achilles Heel

This is where the black swan risk emerges.

Some banks, pressured by inverted curves and negative spreads, need liquidity more than ever.

But other banks, faced with duration mismatches thanks to a surge in ARMs, are withdrawing liquidity from the system by shrinking balance sheets.

That combination is dangerous. In 2008, it wasn’t just subprime loans that brought the system down…it was the freeze in interbank liquidity.

Once banks stopped trusting each other, the whole system nearly collapsed.

Could we be setting up for a similar dynamic? The insider I spoke with thinks so.

History doesn’t repeat, but it does rhyme…and the rhyme this time is liquidity.

If one bank sneezes while another is already holding its breath, the interbank trust chain snaps.

In 2008, it was mortgage paper.

In 2025, it could be something even more mundane: mismatched liabilities and vanishing liquidity. The punchline? By the time you see the headline, the plumbing is already frozen.

Why You Haven’t Heard About This

Most people…even most professional economists…don’t think about the liability side of bank balance sheets in terms of corporate borrowings.

They don’t think about how ARMs change asset duration. And they certainly don’t connect those dots to systemic liquidity.

But the people inside the primary dealer banks do. They’re the ones hedging, managing duration, using swaps and derivatives to keep the system balanced.

And if they’re worried, you should at least pay attention.

The mainstream narrative never touches this because it’s “too complicated” for prime time.

But the insiders know…and they’re already hedging.

When the smartest players in the room shift their risk models, you have to wonder: what do they see coming that the rest of us won’t realize until it’s too late?

The Fed’s Impossible Position

Put yourself in Powell’s shoes:

Keep rates high → the belly of the curve stays inverted, and banks suffocate under negative spreads.

Cut rates → some banks get relief, but others face negative cash flow from fixed liabilities while their assets shorten in duration.

Either way, systemic stress rises. And all of this is happening against a backdrop of slowing growth, declining CPI, and political pressure heading into 2026.

It’s not hard to see how a “routine” rate cut cycle could accidentally trigger a banking liquidity crisis.

Every lever Powell can pull is wired to a trap door. Keep rates high, and the banks suffocate.

Cut rates, and the mismatches accelerate. It’s a lose-lose paradox, and the Fed is cornered.

Which means the real question isn’t whether they’ll make a mistake…it’s which mistake they’ll make first.

Investor Takeaways: Anti-Fragility Over Ignorance

This isn’t about predicting the exact timing of a crisis. Nobody knows that.

It’s about acknowledging risks that 99.9% of investors aren’t even aware exist.

If you’re blindly putting money into an S&P index fund because that’s what your neighbor or Jim Cramer says to do, you’re playing the ostrich strategy.

Head in the sand, hoping the storm passes.

That’s not how contrarians operate. That’s not how you build anti-fragility.

Some principles to keep in mind:

Liquidity is king — In times of stress, the ability to access cash or liquid assets matters more than yield.

Diversify duration — Don’t get caught in the same trap banks are in. Balance short- and long-term exposures.

Watch the plumbing — Pay attention to interbank stress, repo markets, and credit spreads. These are the real early-warning systems.

Expect the unexpected — By definition, black swans come from outside the consensus. If nobody’s talking about it, that’s where the risk probably lies.

Most investors will laugh this off until CNBC tells them otherwise.

But the contrarians…the ones paying attention to liquidity, repo stress, and interbank cracks…they’ll already be positioned.

When the black swan takes flight, the herd scrambles. The prepared don’t. The only question is: which side of that line will you be on?

The Bottom Line

The Fed’s challenge isn’t just inflation and jobs.

It’s a banking system under the surface that may already be relying on a stealth bailout…one that carries its own risks of sparking the next crisis.

If the insider framework is right, the very act of trying to save the system could end up destabilizing it.

As always, you don’t need to panic. But you do need to prepare.

The time to think about these risks is before they hit the front page of the Wall Street Journal…not after.

Because when liquidity dries up, it’s already too late.

The banking system doesn’t blow up when CNBC tells you it might. It blows up when nobody is watching.

And right now, the mainstream media is asleep at the wheel while insiders whisper about liquidity mismatches, asset duration traps, and stealth bailouts already underway.

That’s why contrarians win. They don’t waste energy trying to guess the exact day a crisis hits.

They prepare in advance…with liquidity, diversification, and a map of risks the herd doesn’t even see.

And here’s the truth: the dots we connected today are just the beginning.

The real story is evolving week by week inside the plumbing of the financial system… repo desks, dealer balance sheets, credit markets. That’s the world most investors never access.

But you can.

👉 Join the thousands of liberty-minded, contrarian investors already plugged into the Rebel Capitalist News Desk.

Every week, we cut through the noise to show you what’s really happening beneath the surface…before it becomes front-page news.

Don’t wait until the black swan is already in flight. Prepare now.

🔴 Subscribe to Rebel Capitalist News Desk on Substack and make sure you’re getting the insights that Wall Street insiders don’t share on TV.