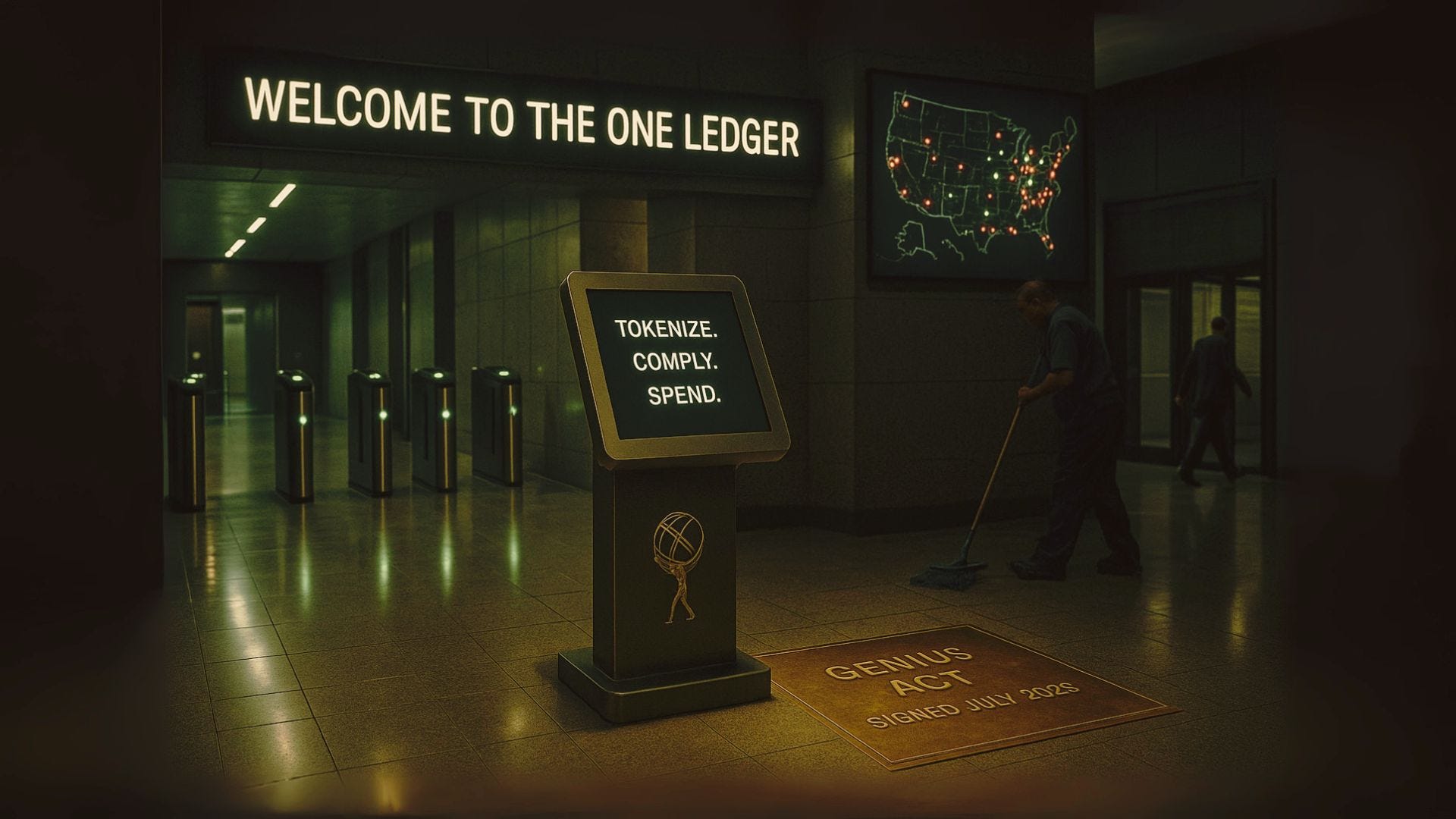

The Genius Act's Hidden Agenda

How Stablecoins Could Morph Into a Centralized Surveillance Grid

Written by Rebel Capitalist AI | Supervision and Topic Selection by George Gammon | July 29, 2025

When the Genius Act was first introduced, it seemed like another regulatory step aimed at keeping up with crypto innovation.

But after a recent conversation with a top expert on digital currency systems, it became clear: this legislation might just be the trojan horse for a fully centralized, programmable monetary grid.

In other words, the Genius Act could lay the foundation for a de facto central bank digital currency (CBDC) system…without ever calling it that.

The One-Ledger Problem

To understand the risks, we need to talk plumbing. Specifically, the plumbing of our current financial system versus a future CBDC system.

Right now, transactions go through commercial banks.

Each bank has its own ledger, and transactions settle on the Fed’s balance sheet using bank reserves. There’s no single, unified ledger.

That fragmentation protects us.

But with the rise of stablecoins and the Genius Act’s new rules, we’re creeping toward a world where everything…every transaction, every identity, every balance…is settled on a single ledger.

Whether that ledger sits at the Fed, JP Morgan, or some other "approved" entity, it centralizes power in a way that should concern anyone who values freedom.

That fragmented plumbing we take for granted today?

It might soon be a relic of the past. And if you think that’s just about efficiency, think again…because the next clause of the Genius Act reveals the true agenda…

The Genius Act's Real Killer Clause

Here’s the bombshell: The Genius Act prohibits non-bank stablecoin issuers from paying interest.

Meanwhile, bank-issued stablecoins (like JPM Coin) are free to offer yield.

This doesn’t just tilt the playing field. It nukes it.

Imagine two coins…Tether and JPM Coin. One pays you 3% to hold it. The other pays zero. Guess which one becomes the standard?

The Genius Act creates an environment where only licensed banks (and more importantly, those who get the blessing of regulators) can dominate the stablecoin space.

That means more power for incumbents, fewer options for consumers, and more surveillance opportunities for the state.

This isn’t free market innovation…it’s monetary gatekeeping with a Silicon Valley UX.

And the deeper you dig into how this clause plays out in practice, the clearer the endgame becomes: a financial monopoly in all but name.

Monopoly by Design?

Let’s say everyone moves to JPM Coin because it’s the only one paying interest and has wide adoption.

Eventually, all transactions settle through JP Morgan’s internal ledger. And now, all you need to surveil, freeze, or manipulate money is access to that ledger.

Worse yet, add a data aggregation layer (like Palantir) and an AI system trained on every transaction... and you’ve got the architecture for a social credit system.

Surveillance capitalism meets central banking.

But don’t worry…they’ll call it "convenience."

As for the real capabilities this setup enables? You won’t find them in the brochure… but you will find them in the next section.

The Slippery Slope to Programmable Money

Stablecoins are supposed to be a convenience.

But once everything is tokenized, and those tokens are issued by a small group of tightly regulated institutions, the temptation to program that money becomes overwhelming.

Want to ensure someone spends their money on food but not gas? Easy.

Want to stop a transaction because it violates "community guidelines"? Done.

Want to freeze someone’s assets for saying something unpopular on Twitter? No problem.

At this point, it’s no longer speculation. It’s architecture. And the most elegant part?

The Fed never even has to launch a CBDC to achieve full-spectrum control. Here’s why.

No Need for a FedCoin

This is the genius (and danger) of the Genius Act: the government doesn’t have to issue a FedCoin.

They just need to regulate the market so thoroughly that only their preferred players survive.

Once everything is on a few interoperable ledgers, it doesn’t matter whose name is on the token. The infrastructure for surveillance is already in place.

So if you’re waiting for a “FedCoin” press release to ring the alarm bells, you’ve already missed the moment.

But here’s where things get even more dangerous…because monetary control might not stop at surveillance.

It might redefine inflation itself.

Double Counting and Money Supply Risks

One more kicker: if stablecoins can be backed by either Treasuries or bank reserves, the Fed may gain direct control over broad money.

That changes everything.

In today’s system, the Fed creates base money (bank reserves) and hopes banks lend it into existence as broad money. But if stablecoins backed by reserves are treated as broad money, then a Fed action (like QE) can suddenly create broad money directly.

That’s a recipe for inflation on steroids.

The plumbing isn’t just changing…it’s mutating. And if this transformation is allowed to accelerate, it could unleash a feedback loop of inflation no one is pricing in.

Let’s zoom out and look at the bigger picture…

Where This Goes Next

If unchecked, this system could:

Concentrate all monetary transactions on a few centralized ledgers.

Allow private corporations (working hand in glove with government) to enforce monetary policy.

Enable real-time surveillance and control of spending.

Expand the money supply far more aggressively than today’s system allows.

And it all starts with a bill called the Genius Act…which most people haven’t even heard of.

What to Watch For:

Stablecoin dominance: If JPM Coin starts gaining market share rapidly, it’s time to pay attention.

Palantir partnerships: If they start linking up with stablecoin providers, you know where the data is going.

Interest-bearing tokens: Watch how regulators approve or deny applications for interest-paying coins.

Retail adoption: The faster merchants and users shift to bank-issued tokens, the faster this system becomes inescapable.

The dots are all there. The ledger. The tokens. The data pipes. The incentives. The question now isn’t if we’re heading toward a centrally managed digital grid…but how fast we get there… and who gets left behind.

Final Thought

The road to CBDC isn’t paved with government coins. It’s built on legislation like the Genius Act, which quietly reshapes the architecture of money under the guise of innovation.

If you care about privacy, decentralization, or even just monetary competition, it’s time to wake up.

If you found this breakdown valuable, subscribe to the Rebel Capitalist News Desk on Substack for deeper dives, expert interviews, and the macro intel you won’t hear on CNBC.

Thousands of liberty-minded readers already trust us…are you missing out?

👉 Join us today and start thinking like a rebel.