The Tweet That Crashed Oil Just Told You Everything About the Real Economy

Oil didn't flash crash. It accidentally told the truth. Strip out the Strait of Hormuz premium and you're looking at $60 oil...on a good day.

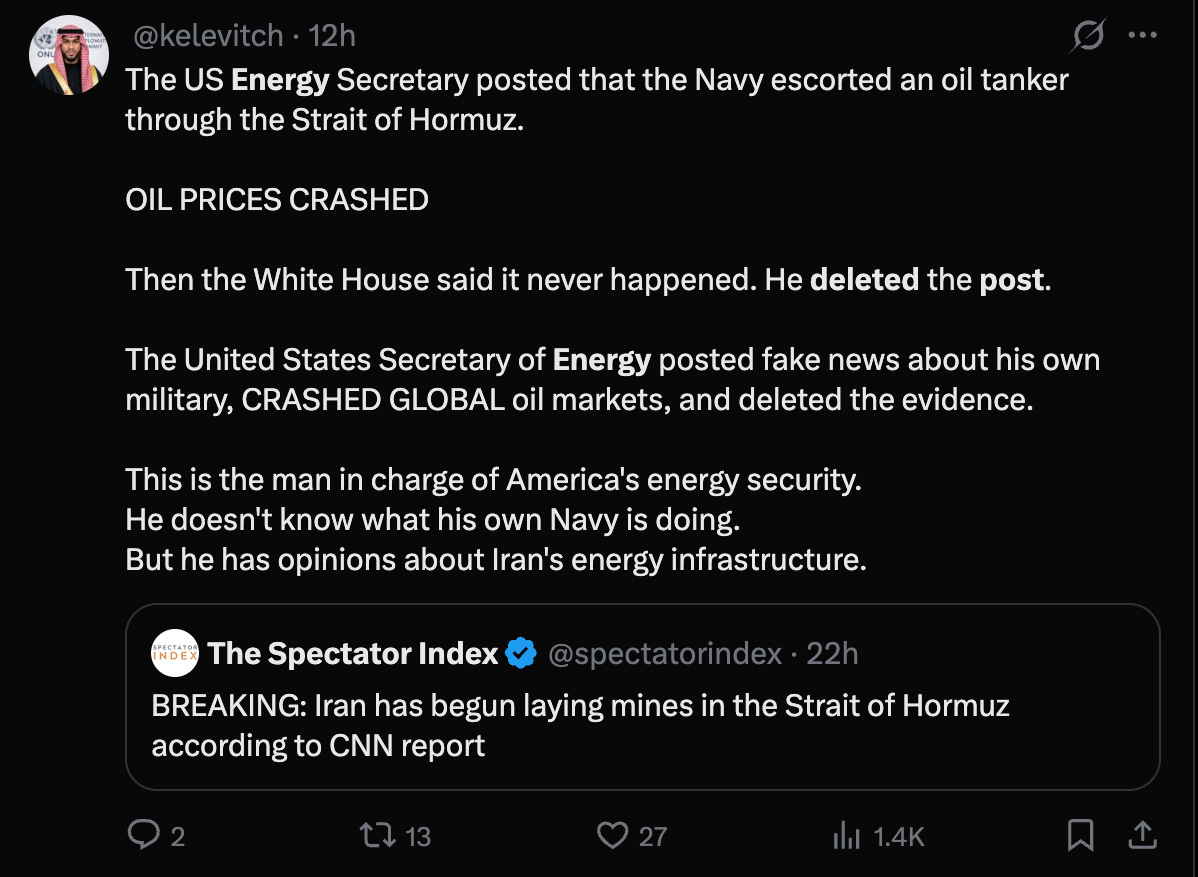

Oil was trading around $84, $85 a barrel. Then, in roughly the time it takes to read a social media post twice, it cratered to a $76 handle. Not over hours. Not over days. Seconds. One of the most essential commodities on the planet was trading like a meme stock...like Dogecoin on a Tuesday afternoon.

The cause? A single post on X from the U.S. Energy Secretary indicating the U.S. Navy had escorted an oil tanker through the Strait of Hormuz. A few uncomfortable minutes passed. Then someone apparently made a very uncomfortable phone call. The tweet disappeared. The Secretary’s page went dark. And oil ripped back above $81 almost as fast as it had fallen.

CNBC scrambled. Anchors were pulling each other back in front of cameras mid-segment. “The post does not exist,” one reporter said, reading back what the platform told her. The intraday low was $76.73. By the time the deletion was confirmed, WTI was already recovering. The whole episode, start to finish, lasted minutes.

Now, the mainstream take is that this was a bizarre one-off...a government communications fumble that created a momentary pricing glitch. Move on, nothing to see here.

That’s the wrong read. Completely wrong. Because the flash crash didn’t create a distortion in the oil price. It accidentally revealed one that was already there.

So what does the size and speed of that move actually tell you about the $84 oil price that existed before the tweet ever went out?

Drum Roll Please: The Hidden Number Inside That Price

Let’s think this one through.

Before the Middle East conflict escalated, the U.S. economy was already showing its seams. Non-farm payrolls printed at negative 92,000. Private credit markets were starting to wobble in ways that don’t make the front page until they absolutely have to.

The broader backdrop...tariffs, slowing global demand, a labor market deteriorating faster than official narratives were admitting...pointed toward weakening energy consumption, not strength. None of that is a setup for $85 oil.

So where would oil actually be trading if you stripped out the Strait of Hormuz premium entirely? Based on what the flash crash just showed, the answer is: a hell of a lot lower. Probably the low 60s. Possibly the 50s. That deleted tweet didn’t represent a seven or eight dollar move in oil. It represented a window into the number that was hiding underneath the geopolitical noise all along.

Come on now. You don’t need a PhD to see what just happened. The market showed its hand. A single disappearing post shaved seven or eight dollars off the barrel price in seconds, then put it back just as fast when the geopolitical risk was re-affirmed by its absence. That is not normal commodity volatility. That is a market being held together by a premium that could evaporate on a single press conference.

And here’s why that matters far beyond the oil price itself.

High oil is a tax. Let’s take it to an extreme to make the mechanics plain: say you bring home five grand a month, $2,500 goes to fixed expenses, and $2,500 is disposable income. Now gas goes to $10, $15, $20 a gallon. What happens to that disposable income? It gets gutted. Down from $2,500 to maybe $1,000. That purchasing power doesn’t disappear quietly ... it gets pulled away from restaurants, retail, services, everything downstream. Producers can’t raise prices to compensate because demand is already falling. So what looked like inflation on the way up becomes the cause of disinflation on the way down. The oil spike that everyone calls inflationary is actually setting up the next leg of weakness. It’s the straw that breaks the camel’s back, and it’s done it before.

This is not a new playbook. The CPI spikes. The Fed gets spooked. Tightening conditions stack on top of an economy already under pressure. And then the very thing that looked inflationary triggers the demand destruction that follows.

The Futures Market Is Reading the Same Script

Here’s another data point that got underreported: oil’s term structure.

Right now, oil is in backwardation...meaning near-term contracts are trading at a meaningful premium to contracts further out. At the peak of the conflict premium, the spread between the front-month and later-dated futures was wide, $10, $15, maybe more. Even after settling back, the December 2026 contract is sitting around $70 a barrel ... roughly $16 lower than the April 2026 contract.

That spread is telling you something. Backwardation of that magnitude in a commodity like oil is not the term structure of a permanent supply disruption. It is the term structure of a market that expects this situation to resolve, and resolve relatively soon. If the market truly believed the Middle East conflict had structurally impaired oil flows for the foreseeable future, December 2026 futures would be trading far closer to April 2026 futures. They’re not. Not even close.

The smart money is pricing in resolution, not escalation. It’s also discounting the demand destruction that a prolonged high oil price would cause ... because the math isn’t complicated. An $85 oil price layered on top of a weakening economy doesn’t sustain itself. It destroys itself by destroying demand.

Futures markets are not always right. But when the flash crash and the term structure are telling the same story...a massive, temporary geopolitical premium sitting on top of a fundamentally weak demand picture...that’s not noise. That’s signal. And right now, both of those signals are pointing in the same direction.

What’s Actually Underneath the Noise

Strip out the Middle East premium and here’s the real economy you’re left with.

Non-farm payrolls at negative 92,000. Under normal conditions...meaning without an oil shock dominating every headline...that number alone would be a market-moving event. It would take oil lower, take interest rates lower, and shift the Fed’s calculus in a meaningful way. Instead, it got buried. The geopolitical premium became the story, and the labor market data became a footnote.

And then there’s the private credit situation, which deserves a lot more attention than it’s currently getting. BlackRock recently halted redemptions in one of its private credit funds above the 5% threshold built into the fund’s own structure. That’s notable. But the more important detail isn’t the halting...it’s the valuation. Assets that were being marked at 100 cents on the dollar just three months ago are now being written down to zero. One hundred cents to zero. In a single quarter.

That is not a rounding error. That is not a market correction. That is a balance sheet that was misrepresenting reality to investors for as long as the tide was in...and now the tide is going out.

As regular readers know, private credit has been functioning as a shadow extension of the credit cycle for years, absorbing risks that traditional banks offloaded and packaging them into vehicles that got marked at par because nobody wanted to price them honestly. Now the marks are starting to tell the truth. My base case is that BlackRock is not the last name on this list. Not by a long shot. The private credit blowup looks like the fifth or sixth inning, not the ninth. There is a lot of tied left to go out.

Here’s how all of this connects back to the Fed. Right now, the central bank is frozen.

The oil spike has pushed short-term inflation expectations high enough that a rate cut at the next meeting looks like a non-starter. The market is pricing in essentially zero probability of a cut in the near term. But that calculus flips the moment the geopolitical premium starts unwinding. When oil drops, yields drop with it, and the NFP data comes back into focus, the probability of Fed cuts in the second half of 2026 rises fast. The market reprices. Quickly.

What to Watch...and Where the Setup Lives

The two-year Treasury is the tell here.

At roughly 3.6%, the two-year is baking in close to zero probability of Fed rate cuts. The market is saying: inflation is still the dominant risk, oil is still elevated, and the Fed isn’t moving. That is the current price of the geopolitical premium, expressed in yield terms.

That picture changes fast if and when the situation in the Strait resolves. And here’s the political reality: Trump will claim victory. Whether the underlying facts support the claim is a separate question entirely...and one that will not slow him down for a single moment. The narrative will be packaged, the press conference will be held, and the exit will be declared a triumph. That’s the MO, and recognizing the MO is not a political statement, it’s just pattern recognition.

When that moment comes...and the oil price drops back toward the low 60s, and the geopolitical justification for elevated yields disappears...the two-year Treasury is going to reprice to reflect something closer to the real economy. An economy with a negative NFP print. An economy with private credit stress spreading across balance sheets. An economy where the consumer’s disposable income has been quietly taxed by months of elevated oil. If the probability of Fed cuts moves from near zero back to even 25 or 30%, that is a significant move in the two-year. Not a small one.

There are no certainties here, only probabilities. But the flash crash already gave away more than the mainstream read is crediting. It revealed the size of the premium. The term structure confirmed the market sees it as temporary. The labor market data and the private credit news confirmed the underlying economy was already softening before any of this started.

Watch the Strait of Hormuz for signs of re-opening. Watch the oil term structure...if the backwardation starts flattening, that’s the early signal the premium is unwinding. Watch the private credit headlines, because BlackRock is the canary and the coal mine goes a lot deeper than one fund. And watch the two-year yield, because when it starts moving, it will not move slowly.

Facts > Narrative. The flash crash already told you what the narrative was hiding.

Stand up for freedom, liberty, and free market capitalism.

I wonder how Trump claiming a bogus victory will help to open Hormuz without US withdrawing completely from Middle East and paying reparations to Iran?