Trump vs. Powell?

Behind the Rate Drop, Two Signals the Market Can’t Ignore

Written by Rebel Capitalist AI | Supervision and Topic Selection by George Gammon

July 17, 2025

Markets moved sharply yesterday…but not for the reasons most people think.

Yes, PPI came in well below expectations. Yes, Trump is reportedly considering firing Jerome Powell. The signal is clear: expectations for easier monetary policy are climbing, and fast.

Question is no longer “Will the Fed cut?” It’s “What happens if Trump reshapes the Fed itself?”

Let’s unpack what happened.

PPI: Inflation Isn’t Just Under Control…It’s Slowing

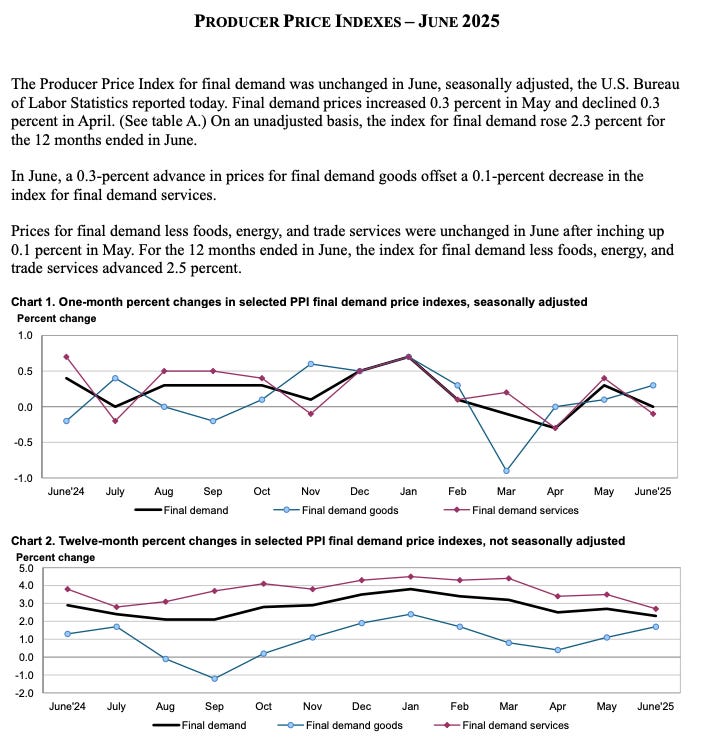

The June Producer Price Index (PPI) was a major surprise:

Headline MoM: 0.0% vs 0.3% expected

Core MoM: 0.0% vs 0.2% expected

YoY Headline: 2.3% vs 2.7% prior

YoY Core: 2.5% vs 2.8% prior

This wasn’t a “softening” report...it was a collapse in pricing pressures, suggesting producer-level inflation is cooling even more rapidly than consumer prices. That’s a strong disinflation signal.

Markets reacted accordingly. Treasury yields initially fell across the curve, pricing in weaker inflation and growing odds of a Fed cut. But then, the narrative shifted dramatically.

Just as traders were recalibrating rate expectations off the data, a political earthquake hit the tape…one with potentially far greater consequences than a benign inflation print.

Trump vs. Powell: The Political Bombshell

Shortly after the PPI data, Bloomberg dropped a report that shook D.C. and Wall Street: President Trump is considering firing Fed Chair Jerome Powell.

While this move would almost certainly spark legal and political backlash, the market doesn’t care about constitutional nuance...it cares about interest rates.

And Trump has made his stance crystal clear: he wants rates 300 basis points lower.

That would take the Fed Funds Rate from today’s 4.25% down to 1.25%. And if he’s serious about removing Powell to get there, the bond market is going to take notice.

If this was just campaign-season rhetoric, markets might’ve shrugged it off.

But the bond market moved...and that tells you everything you need to know about how seriously investors are taking the threat.

How the Market Reacted

Let’s talk numbers:

10-Year Treasury Yield: Down ~2.5 basis points

2-Year Treasury Yield: Down ~5.5 basis points

Yield Curve: Steepened by ~3 bps

The key here is the front end. The two-year yield...which is more closely tied to expectations for Fed policy...fell more than the ten-year. That steepening suggests the market is increasingly confident that short-term rates are coming down.

And that front-end move isn’t happening in a vacuum. It’s a signal that belief—not legality...is driving market mechanics. Which brings us to the next uncomfortable truth…

Legal or Not, the Market Thinks It’s Real

Can Trump legally fire Powell? That’s debatable. Most legal scholars argue the Fed chair can’t be removed without cause.

But in the real world, markets don’t trade on law books...they trade on perceived probabilities. If investors believe Trump might fire Powell, and that whoever replaces him will be dovish, that changes expectations right now.

And that’s exactly what we’re seeing in yields.

Whether Powell stays or goes may ultimately be settled in court. But in the meantime, the market is voting with its feet...and it's not waiting for a judge to weigh in.

The Fed's Credibility Crisis

Let’s not forget: the Fed is already under pressure.

With core inflation below 3%, personal consumption softening, and M2 money supply flat since 2022, there’s little justification for the Fed’s continued hawkishness...except for the appearance of control.

If Trump forces Powell out, or even creates enough uncertainty to erode confidence, the Fed’s forward guidance could lose credibility entirely. That would likely accelerate bond market moves and potentially create broader volatility.

And if credibility slips, the consequences won’t be limited to yields. They’ll ripple across risk assets, currencies, and potentially into the political arena itself. We’re already seeing early signs of that convergence.

PPI + Powell = Perfect Storm?

Taken together, the disinflationary PPI print and the Trump-Powell drama form a potent cocktail. One lowers the inflation outlook, while the other raises the odds of aggressive rate cuts.

In a vacuum, either might nudge yields lower. Together, they sent a clear signal: easier monetary policy is coming, one way or another.

The result? A rate-reset narrative taking hold...fast. And for those positioned for curve steepening, the payoff is starting to show.

Steepener Trade Paying Off

If you've been following the spread trade we discussed recently...the bet that the yield gap between 2-year and 10-year Treasuries will widen...you had a great day.

As George has said repeatedly: this isn’t just about predicting direction. It’s about understanding how the curve moves.

When the short end drops faster than the long end, that’s the market betting on lower front-end rates due to policy shifts…not long-term economic strength.

But this story isn’t just about trades…it’s about perception. And one PR disaster inside the Eccles Building is throwing gasoline on an already smoldering fire.

The Renovation Scandal: More Than Optics

The $2 billion Fed building renovation project has become a lightning rod in this debate. Trump and allies argue that spending taxpayer-linked funds on luxury offices during a time of economic strain is out of touch.

And they may have a point.

The Fed is running negative cash flow, paying more in interest on reserves than it earns on its asset portfolio. That means those “profits” that usually go back to the Treasury...and by extension, the taxpayer…are now being redirected to banks like JPMorgan.

In that context, spending billions on Fed offices looks politically toxic. Whether or not it’s legally relevant, it’s optically damaging. And in politics, optics often drive outcomes.

Optics may not move CPI or GDP, but they can shift political will..and political will can move central banks. Especially when the walls of the Fed’s $2 billion palace start to feel paper-thin.

Final Thoughts

This isn’t just about a PPI print. It’s about a shift in market psychology—driven by data, politics, and a growing sense that the Fed’s grip on monetary policy is slipping.

If Powell is fired, or even if the threat of his firing causes enough instability, we could see rate expectations reset quickly. But even without the political drama, the PPI data alone suggests the Fed is behind the curve.

Trump’s push for lower rates may be brash, but it’s not entirely untethered from macro reality. Inflation is falling. Growth is weak. And the Fed’s stance is looking increasingly outdated.

The takeaway?

Inflation is not the primary risk.

Political interference may accelerate policy shifts.

The market is beginning to front-run both outcomes.

In this environment, staying nimble isn’t optional…it’s essential.

🚨 Become a paid subscriber and join George Gammon for his Friday weekly wrap-ups and more…