Will The Federal Reserve Need A Bailout?! (Yes…Here’s Why)

A Financial Apocalypse Lurking in The Shadows

Hold onto your hats, folks, because the ground beneath the financial markets is far less stable than it appears. No, this isn’t a thriller plot, and I haven’t hired a Hollywood scriptwriter. This is the cold, hard reality, and the main protagonist—brace yourselves—is none other than the Federal Reserve. That’s right, the very institution designed to prevent financial meltdowns could be on the verge of needing a bailout itself. The question isn’t “if” but “when.”

A Cautionary Tale from Sweden

Before you dismiss this as an over-the-top hyperbole, consider the story of Sweden’s central bank, the Riksbank. This isn’t some banana republic’s financial debacle; it’s the world’s oldest central bank, and it’s facing a situation so dire that it has officially approached the Swedish government for a bailout. The Riksbank is, as we speak, technically insolvent. What happened? A simple yet devastating rise in interest rates exposed the flaws in their balance sheet, causing a loss of public and market confidence.

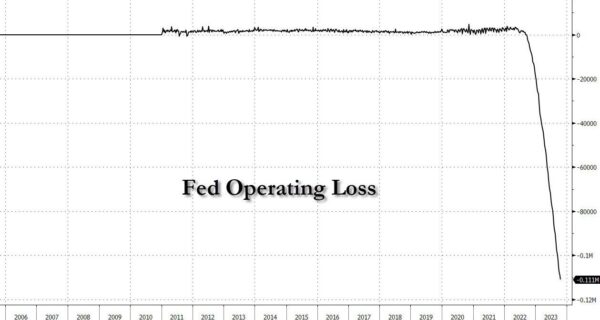

The Fed’s Perilous Position: A House of Cards

You might argue that the Federal Reserve and the Riksbank are apples and oranges. But here’s the kicker: the Fed’s situation mirrors the Riksbank’s but on a grander and more dangerous scale. The Fed has suffered losses to the tune of $110+ billion just over the last few months. Now, you might say, “Isn’t the Fed immune to bankruptcy?” Technically, yes, but in reality? Maybe not.

The Asset-Liability Mismatch: A Financial Abyss

The Fed earns money from the interest on the assets on its balance sheet. But it pays out as expenses the interest on reserves to banks. So, when the Fed hikes up interest rates—say, to 5.25%—while earning perhaps only 1.5% on its assets, the math puts the Fed squarely into the ‘no bueno’ zone. It’s like earning $50,000 a year while your expenses are $100,000. You don’t need to be a Wall Street guru to know that’s a fast track to insolvency. The Fed employs accounting gimmicks, like “deferred assets,” to offset these losses. This deferred asset is essentially the Fed saying, “We’ll make money in the future, so let’s count it now.” In other words, it’s a financial illusion, a sleight of hand.

One aspect of Federal Reserve Bank accounting that will be important in some scenarios is

Federal reserve board

the deferred asset. When Reserve Bank income is not sufficient to cover interest expense,

realized losses, operating and other expenses, a deferred asset is created.

The Ultimate Weapon and Achilles’ Heel: Confidence

Here’s the linchpin: the Federal Reserve, like any other institution, survives on confidence. But what happens when that confidence evaporates? Eric, the Jerome Powell of Sweden, hit the nail on the head: a central bank can operate without equity in the short term, but to maintain confidence in the long term is another story.

The Hourglass is Running Out: What Next?

So, the million-dollar question—or should I say, the $110 billion question—is this: When will the Fed lose that confidence? It’s not a matter of if; it’s a matter of when. And when it does, the repercussions will be like a financial tsunami, wiping out not just Wall Street’s sandcastles but potentially the global economy.

The Fed might be the Wizard of Oz now, but remember, even wizards can’t escape reality forever. So, whether you’re a Wall Street veteran or just an Average Joe, keep a vigilant eye on the Fed. Because once that curtain is pulled back, there’s no telling how far the dominoes will fall.