You See This Right Before A Recession Hits

The Clock is Ticking, and It’s Not Just Ticking—It’s Roaring

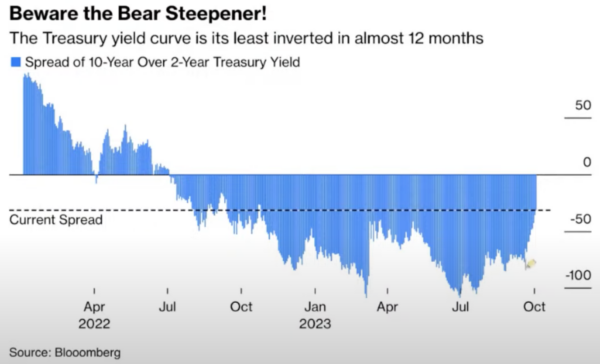

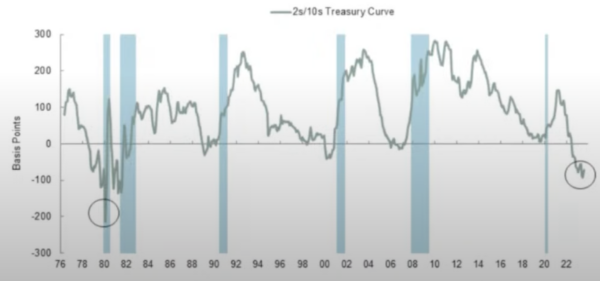

Listen up, folks! If you think the inverted yield curve was a red flag, brace yourselves. We’re now staring down the barrel of a “bear steepener,” a phenomenon that could be an even more ominous harbinger of economic doom. This isn’t just a warning sign; it’s a five-alarm fire. So, what’s the big deal? Let’s dive in.

What is a Bear Steepener?

In the financial world, the yield curve is often seen as a crystal ball, predicting economic conditions. A “bear steepener” occurs when the long end of the yield curve rises, tightening the gap between short-term and long-term yields. Sounds technical? Let’s break it down: it means that the cost of borrowing for the long term is going up, and that’s not good news for anyone.

The Bloomberg Article: A Mixed Bag

A recent Bloomberg article by John Authers discussed this very topic, but it was a bit of a rollercoaster. Authers started strong, highlighting the dangers of a bear steepener, but then veered off course. He seemed to suggest that the yield curve’s predictive power might be losing its edge. But is that really the case?

The Fatal Dis-Inversion: A Misunderstanding?

The term “dis-inversion” has been thrown around a lot, but it’s crucial to understand what it actually means. Authers uses it to describe the gap between the 10-year and 2-year yield decreasing, but not to the point where the curve is no longer inverted. Confused? You’re not alone. The term is misleading. The curve is still inverted; it’s just less so than before.

The Real Indicator: It’s Not Over Until It’s Over

Joe Lavorgna of SMBC Nikko confirms that the curve usually inverts before a recession but is often no longer inverted by the time the recession officially begins. So, are we out of the woods if the curve is “dis-inverting”? Absolutely not. The curve has to fully uninvert, and that hasn’t happened yet.

Cognitive Dissonance and the Arrogance of Central Planning

Why is the yield curve—the financial world’s equivalent of a crystal ball—so glaringly ignored by mainstream economists and media? Could it be that these self-proclaimed oracles are too entrenched in their central planning mindset to admit that the market, that great unwashed mass of traders and investors, might actually be smarter than they are? It’s a bitter pill to swallow, especially when your entire academic and professional life has been built on the premise that you are the intellectual elite. Admitting that the market is right would be tantamount to flushing their PhDs down the toilet.

The Market’s Unheeded Warning

The yield curve is not just some arcane financial metric; it’s the market’s siren call, signaling that something monumental is on the horizon. Ignoring it is like disregarding a tornado siren because you find the sound too jarring. It’s not just irrational; it’s a perilous game of Russian roulette with economic stability.

Selective Hearing and the Danger of Outdated Information

And let’s not forget the audacity of some authors who cherry-pick outdated articles to support their narrative. One such author even linked to an old article suggesting that the yield curve might be a “false indicator,” while conveniently ignoring more recent articles that affirm rising recession odds. It’s like a climate change denier pointing to a snowstorm as proof against global warming, while ignoring the overwhelming evidence of rising global temperatures.

The yield curve is not just some financial doodle; it’s a harbinger of economic conditions to come. It’s time to stop this willful ignorance and acknowledge that the collective wisdom of the market far exceeds the knowledge of any PhD at the Fed.