The 2-year Treasury just made a 30-basis-point move in five days.

That is not noise. That is the bond market telling you something...and right now, it’s telling you that the Fed’s rate-cutting cycle might be over before it properly started. When the two-year yield traded as high as 3.97% intraday on Thursday against a Fed funds range of 3.5% to 3.75%...you had a market that, for a brief moment, was pricing in the possibility of a Fed rate hike. Not a pause. An actual hike.

Let that sink in.

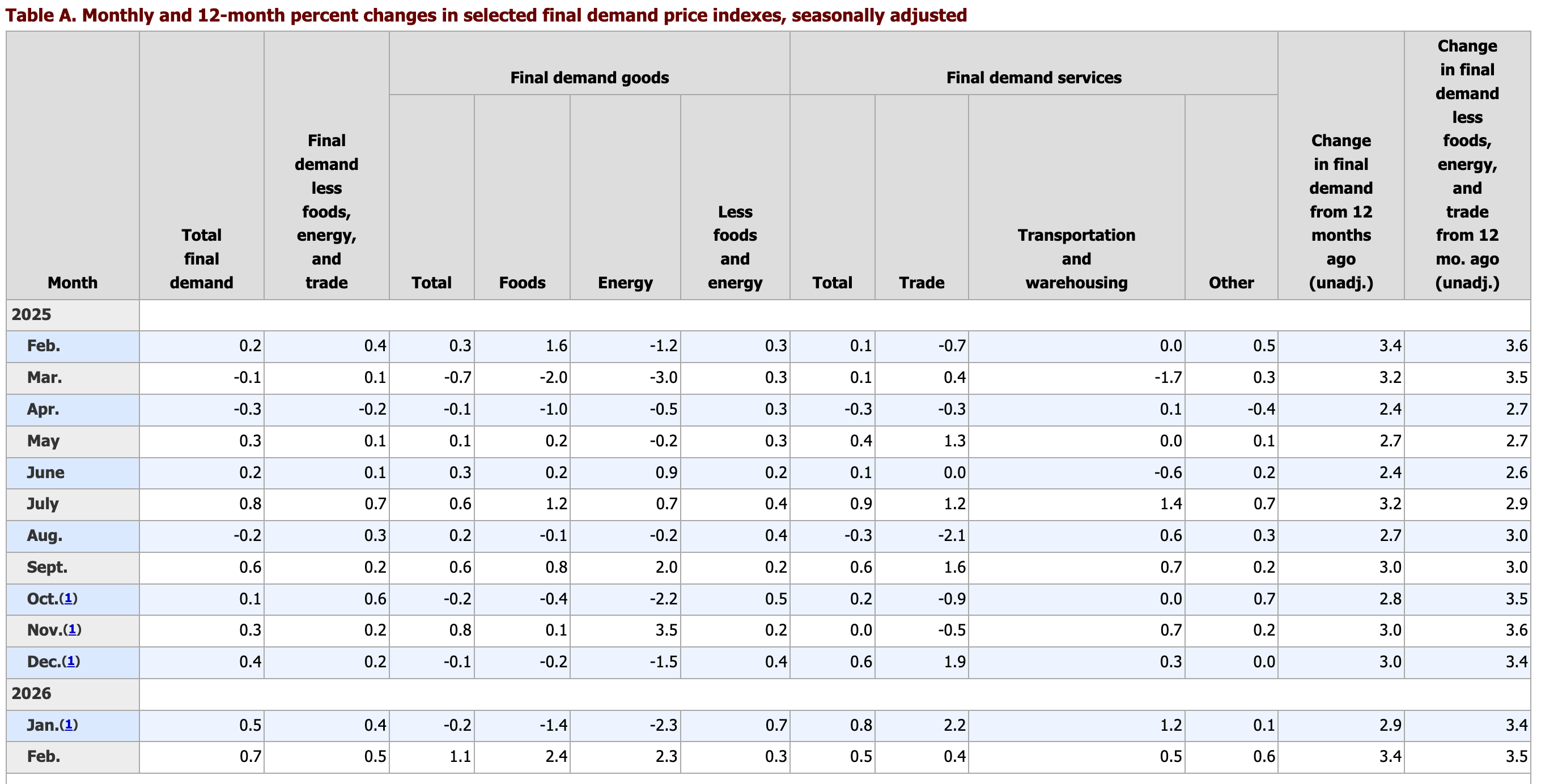

The catalyst wasn’t hard to find. On Wednesday, the BLS dropped the February Producer Price Index...and it wasn’t pretty. Headline PPI came in at 0.7% month-over-month against an expectation of 0.3%...more than double what economists had penciled in. On an annual basis, wholesale inflation jumped to 3.4%, the highest reading in a year. Then Thursday morning, initial jobless claims came in at 205,000 for the week ending March 14, beating the expected 215,000...the lowest level since January...and the two-year ripped right back toward 4%.

The stagflation trade was fully on.

Add in a war in the Persian Gulf that has crude oil trading at multi-year highs, a Fed that just delivered a hawkish hold while admitting publicly it can’t project anything with confidence, and a bond market now assigning a non-trivial probability to the unthinkable...and you’ve got a financial environment that is, in almost every detail, a photocopy of the summer of 2008.

So the question isn’t whether the market is right to panic about inflation. The question is whether it’s looking at the right historical playbook...because the last time this exact setup played out, the central banks that raised rates to fight the oil shock didn’t just get it wrong. They created the preconditions for the worst deflationary collapse since the Great Depression.